What are Member Contributions?

Most New York State and Local Retirement System (NYSLRS) members contribute a percentage of their gross earnings to the New York State Common Retirement Fund (Fund). These member contributions, in addition to employer contributions and investment earnings, help make sure the Fund stays well-funded to support the retirement benefits earned by members and retirees.

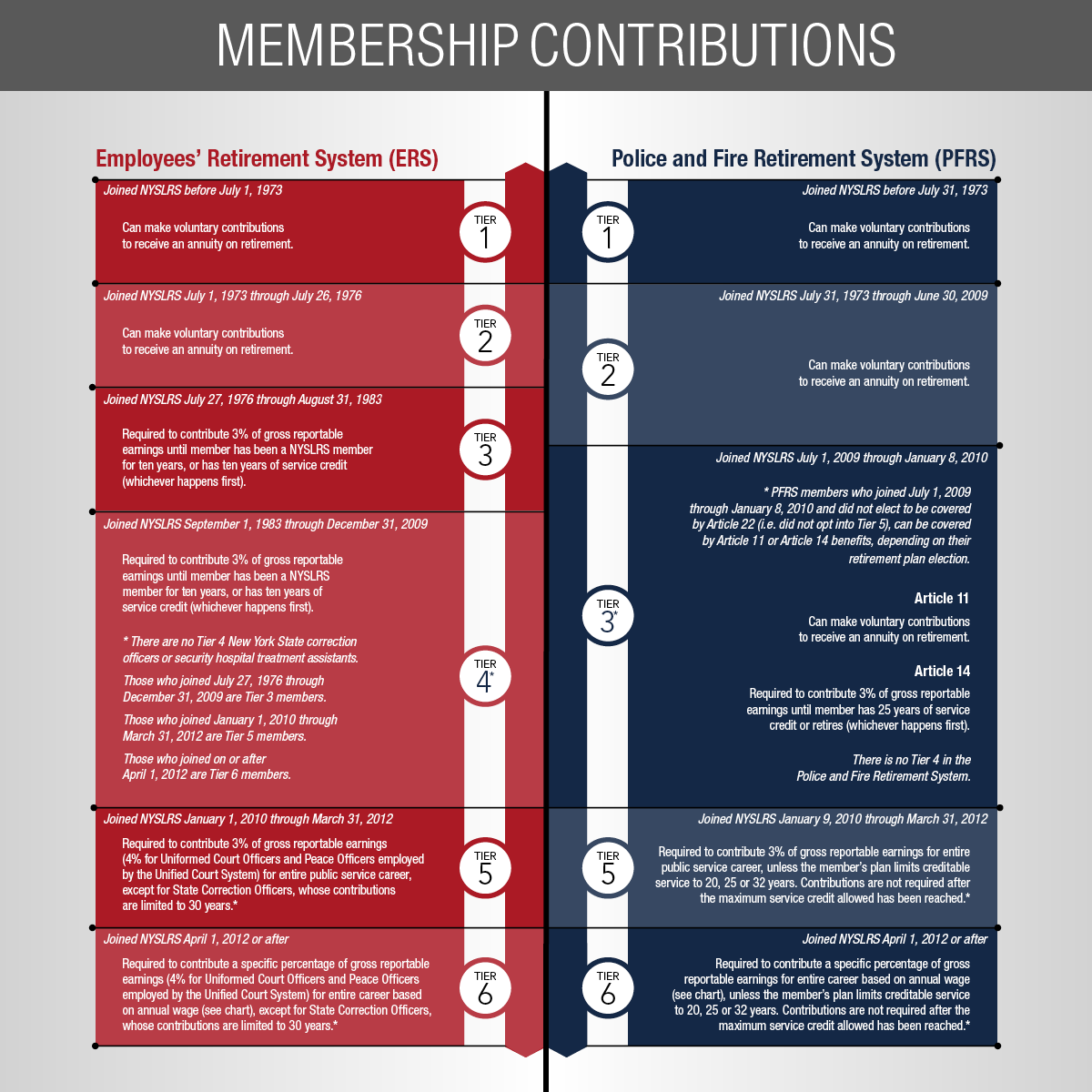

Types of Member Contributions

Your tier and retirement plan determine if you must contribute and what percentage of your earnings you contribute. At NYSLRS, there are two types of member contributions: required and voluntary. If you belong to a retirement plan with required contributions, you must make member contributions for the length of time stated in your retirement plan. If you make voluntary contributions, you belong to a retirement plan where you don’t have to make contributions, but you can volunteer to make contributions.

Your tier and retirement plan determine if you must contribute and what percentage of your earnings you contribute. At NYSLRS, there are two types of member contributions: required and voluntary. If you belong to a retirement plan with required contributions, you must make member contributions for the length of time stated in your retirement plan. If you make voluntary contributions, you belong to a retirement plan where you don’t have to make contributions, but you can volunteer to make contributions.

To help you understand how much you are supposed to be contributing, here is some useful information regarding contributions, broken down by what system you are in:

Employees Retirement System (ERS)

- Most ERS Tier 1 and 2 members are not required to contribute, but may contribute voluntarily. ERS Tier 1 and 2 members receive an annuity based on their voluntary contribution balance in addition to their pension at retirement.

- All ERS Tier 3 and 4 members are required to contribute 3 percent of their gross earnings until they’ve been NYSLRS members for ten years, or have ten years of service credit (whichever comes first).

- ERS Tier 5 members are required to contribute 3 percent of their gross earnings for their entire career.

- ERS Tier 6 members are required to contribute for their entire career a specific percentage of their earnings based on their salary.

ERS Exceptions

- Though most ERS Tier 5 and Tier 6 members are required to contribute for all their years of service, the contributions of State Correction Officers in these tiers are limited to 30 years of service.

- ERS Tier 5 Uniformed Court Officers and Peace Officers employed by the Unified Court System must contribute 4 percent of their salary for all their years of public service.

Police and Fire Retirement System (PFRS)

- Most PFRS Tier 1 and Tier 2 members, as well as PFRS Tier 3 (Article 11) members, are not required to contribute, but may contribute voluntarily.

- PFRS Tier 3 (Article 14) members must contribute 3 percent of their gross reportable earnings for 25 years or until retirement (whichever comes first).

- PFRS Tier 6 members are required to contribute a specific percentage of their earnings based on their salary for their entire career.

PFRS Exceptions

- Though most PFRS Tier 5 members must contribute 3 percent of their gross reportable earnings for all their years of public service, PFRS Tier 5 members enrolled in a retirement plan limiting the amount of creditable service they may accrue will not be required to contribute once they reach the maximum amount of service allowed by their plan.

- If a union-negotiated collective bargaining agreement in effect on January 9, 2010 required an employer to offer a 20- or 25-year plan, any new employees who join while that agreement is in place will not have to contribute.