Members of the New York State and Local Retirement System (NYSLRS) become eligible for a death benefit after one year of service. However, if you’re a New York State employee (meaning that you work for the State of New York), your beneficiary can also receive a death benefit from the Survivor’s Benefit Program for State employees.

Eligibility Requirements for the Survivor’s Benefit Program

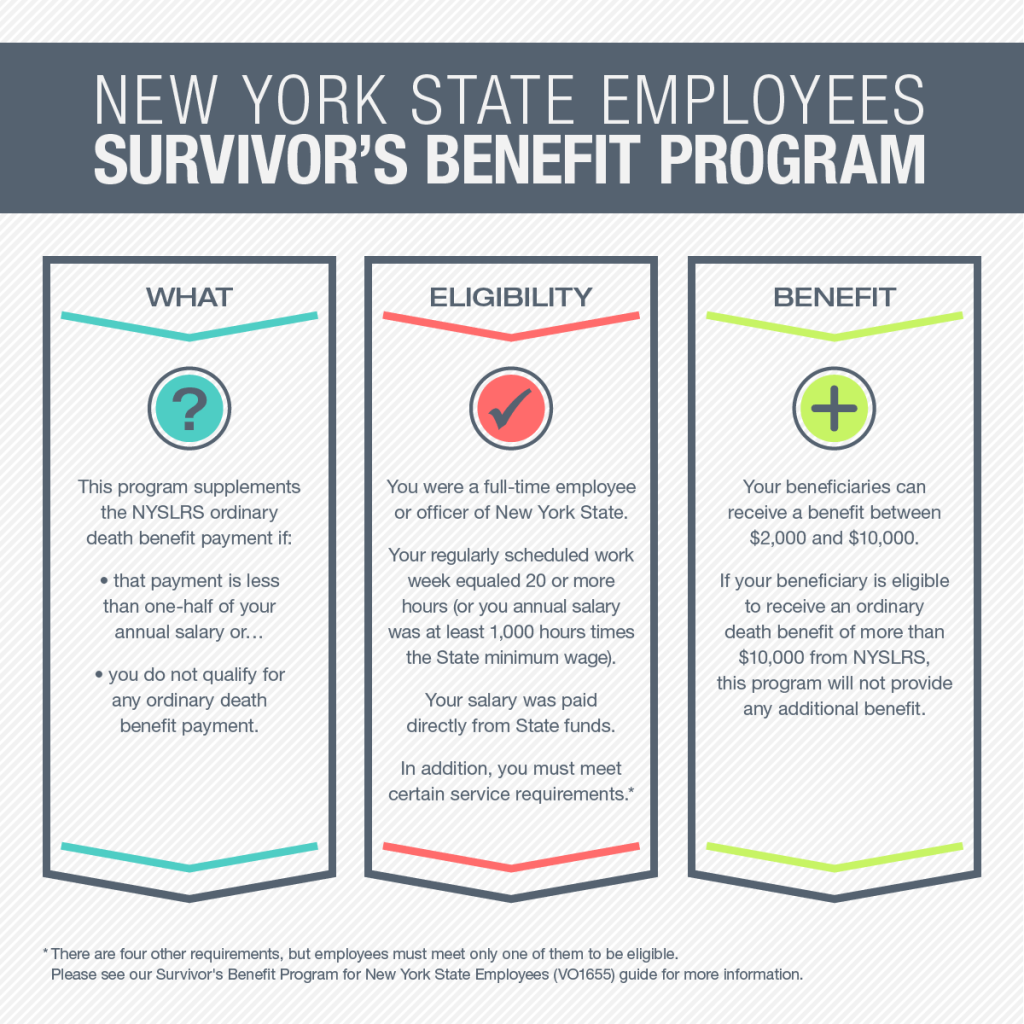

You don’t have to enroll in the program; your beneficiary is eligible to receive this benefit if, at the time of your death:

- You were a full-time employee or officer of New York State

- Your regularly scheduled work week equaled 20 or more hours (or your annual salary was at least 1,000 hours times the State minimum wage) and

- Your salary was paid directly from State funds

There are also other eligibility requirements for the Survivor’s Benefit Program.

How Much Your Beneficiary Will Receive

This program supplements NYSLRS’ ordinary death benefit payment if that payment

is less than one-half of your annual salary, or if you don’t qualify for any ordinary death benefit payment.

The maximum amount payable to your beneficiary is $10,000; the minimum amount is $2,000. Both amounts include the ordinary death benefit paid by NYSLRS plus your survivor benefit. If your beneficiary is eligible to receive a NYSLRS ordinary death benefit of more than $10,000, this program will not provide any additional benefit.

Also, if NYSLRS pays an accidental death benefit, a $2,000 survivor’s benefit will also be paid to your beneficiary.

If you have questions about the program, read our publication, The Survivor’s Benefit Program for New York State Employees. If you have questions about any other retirement-related matters, please contact us.