As a NYSLRS member, your defined benefit pension plan is a good reason to be optimistic about your finances when you retire. Your pension will provide you with monthly payments for the rest of your life. But there is more to a financially secure retirement than having a pension. Understanding your potential sources of income will help you plan for your future and boost your retirement confidence.

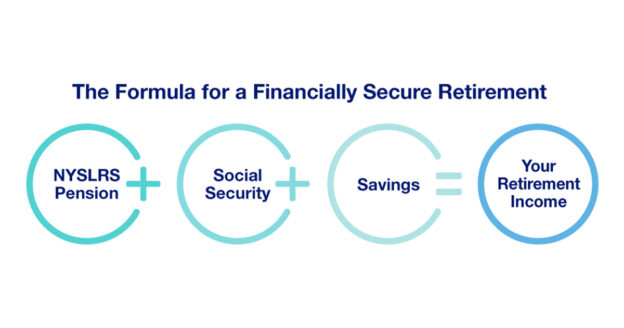

Think of retirement security as a three-legged stool. Each leg is a source of income to help support you when your working days are done.

Leg 1: Your NYSLRS Pension

At retirement, vested NYSLRS members are eligible for a pension based on their final average earnings and the number of years they’ve worked in public service. Your NYSLRS pension provides you with a monthly payment for the rest of your life, no matter how long you live. Unlike workers who rely on a 401(k)-style retirement plan, you won’t have to worry about this income running out.

Most members can use Retirement Online to estimate how much their pension will be. But, if you’re a long way from retirement, it may be better to think in terms of earnings replacement. Financial advisers estimate you’ll need to replace 70 to 80 percent of your income to retire with confidence. Your pension can help get you there. For example, if you retire with 30 years of service, your NYSLRS pension could replace more than half of your earnings. (Pension benefits depend on your tier and retirement plan. Look up your retirement plan publication to find out how your retirement benefit will be calculated.)

Leg 2: Social Security

Your Social Security benefit is another source of income to help support you in retirement. It replaces a percentage of your pre-retirement income. At full retirement age, your social security benefit can replace from about 75 percent for lower income earners to about 27 percent for higher income earners. Visit Social Security’s Plan for Retirement page to estimate your income and learn more about your benefit.

Leg 3: Retirement Savings Can Boost Your Confidence

A lifetime pension and Social Security income will be substantial financial assets, but it’s still important to save for retirement. A healthy retirement savings will give you more flexibility during retirement, helping to ensure that you’ll be able to do the things you want to do. It can also help in case of an emergency and act as a hedge against inflation.

Saving is the retirement factor you have the most control over. You decide when to start, how much to save and how to invest your money. The key is to start saving early so your money has time to grow, even if you can only afford to save a small amount in the beginning.

Eligible employees might consider saving with the New York State Deferred Compensation Plan (NYSDCP). Money gets deducted from your paycheck so you won’t even have to think about it. NYSDCP is not affiliated with NYSLRS, but New York State employees and some municipal employees can participate. If you’re a municipal employee, ask your employer whether you’re eligible for NYSDCP or another retirement savings plan.

Who do I contact regarding final calculation of my pension. I retired effective 4/29/23 . There is a 3% raise from PEF that is not included. ( contract ratified in June 2023) I’ve been emailing via retirement online with no success.

NYSLRS is working hard to complete recalculations and to provide retroactive payments as quickly as possible. During the last year, a large number of retroactive contract settlements and accruals were reported for our retirees and we are still in the midst of making these adjustments. We apologize for the length of time this is taking. Most initial pension payments are made by the end of the month following retirement and are close to a retiree’s final calculation. Thank you for your patience.

one retirement option not mentioned was relocating to a place that is lots cheaper to live … overseas .. unfortunately NYSLR doesn’t support overseas bank account deposits … a severe lacking in a system recently rebuilt to the tune of millions of dollars and with thousands of employees needing to take this option … why are they not being more accommodating to people who have served the public faithfully for years

So your NYS pension can’t be paid into a foreign bank account, but your Social Security can be?

Unfortunately, NYSLRS does not transfer funds into international accounts across national borders.

For information about Social Security payments, please visit the Social Security Administration website.

When I first joined the “retirement” system in 1983 (Tier 4) I was told my retirement would be calculated as follows: Number of years X 2% X your final average salary.

The final average salary would be the average of the 3 highest years. What I understand now is that is not true. After 30 years we only get 1.66% for every year after 30 and that the final average salary cannot exceed 110% of the 4th and 5th highest years. At 32 years, using an estimated income stream, this difference equates to over $14,000 per year in pension loss. That is substantial! If this is all true, I do not believe the terms of one’s pension should be changed in the middle of the game.

Retirement benefits are established by law. NYSLRS administers programs that are signed into law.

You can visit our website to find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits you’re entitled to receive for your specific tier and retirement plan.

If you have questions about your retirement plan benefits, please message our customer service representatives using our secure contact form. Filling out the secure form allows our representatives to safely contact you about your personal account information.

I have all three but started too late in life with the savings. And if I had had enough in savings to retire at age 70 (I’m 76), I’d be better off now.. My advice to my nephews and nieces is to start a personal savings as soon as they start working. I’m advising them to have money automatically transferred to a savings account and increase the amount as their salaries increase. Please target your younger employees with messages like the 3-legged-stool approach to retirement. HR departments should provide seminars for all of their employees with a focus on the younger ees. Thank you for your newsletters.

Thank you for your feedback. We’re glad you enjoy our newsletters.

The Trifecta or 3 legs works so long as each leg holds. Pull down one and you are on the floor. Our elected need to secure and bolster Social Security, NYS Deferred Compensation and the NYS Retirement System. This is especially important for low income public employees and low income public retirees. These individuals and their families are struggling.

The organizations (i.e, NYSOMCE, APRONY, NYSARA, State AFL/CIO, CSEA, NYSAARP, RPEA, NYSCOPA, Teamsters, etc.) representing these folks need to address the problem by managing health insurance costs and selecting a single COLA bill from the pile of unsuccessful COLA bills floated for the past 23 years. This pile of COLA bills unwittingly support the divide and conquer intent and the made to order excuse useful to some elected to deny any COLA bill passage. Their are other excuses in their bag of tricks to prevent the help needed for low income public employees and low income public retirees.

Members make your voices heard in these organizations and get them to break down the self imposed barriers that prevent these organizations from working together on the common ground of COLA and Health insurance.

I couldn’t agree more. The key to financial success starts early in your career. A highly disciplined plan is painful at the start however rewarding in the end I personally had moments of doubt but in the end it was all worth the sacrifices and efforts my suggestion is save like your life depends on it sacrifice whatever is not needed enjoy the ride but don’t think someone is going to do it for you. You’re the master of your own destiny. Buy. House pay it off Get the kids through schools and enjoy.

This “3-legged Stool” has been known as the “Trifecta” of NYS Retirement since the 1980’s, and it’s a good plan to follow…

When is the best time to talk to an retirement coordinator?

A consultation is not required, but if you’re nearing retirement and you have questions, you can speak with one of our information representatives.

NYSLRS provides personalized pre-retirement consultations to members by telephone. You can call 866-805-0990 to make an appointment. The Call Center is open Monday through Friday from 7:30 am – 5:00 pm.

Before a consultation, you may wish to sign in to Retirement Online to review the information we have on file for you, such as your total service credit, and use the online benefit calculator to estimate your pension. If you don’t already have an account, go to the Sign In page and click the “Sign Up” link under the “Customer Sign In” button.

You may also be interested in the retirement timeline on our website. It shows the steps you’ll need to take and highlights important topics and information you’ll need to consider.

Start planning early. I looked into it at 17 yrs on my job . It took 12 years for me to save enough to retire. Back then in 2012 I needed 500,000 in savings to retire on most retirement calculators. . Add 3% a year to that figure. If your retirement income covers your bills for 10 yrs ,you can retire with less ,assuming your savings grows at 10% norms.

Use it, it will be Beneficial, to ALL! Start Early! I waited 11 years. In 24 years, I was able to grow to over $725,000. Would not have been able to do that on, my OWN! Automatically taken, from ALL of your earnings(REG. & OT)

You left out a very crucial fact: The DCP offers not only a pre-tax account but an after-tax Roth account. Please include this important fact in you correction

Never knew that

Thank you for this good advice !

Happy you found it helpful.