Among the most important benefits a NYSLRS membership provides are death benefits. When you’re covered by a death benefit, your beneficiary may receive a payment on your behalf at your death.

Death benefits can vary by tier and retirement plan, so for the purpose of today’s post, let’s focus our attention on the Employees’ Retirement System (ERS) Tier 2, 3, 4, 5 and 6 members in regular plans. (If you’re in a special 20- or 25-year plan or are a Tier 1 member, please review your plan publication to learn more about your death benefits.)

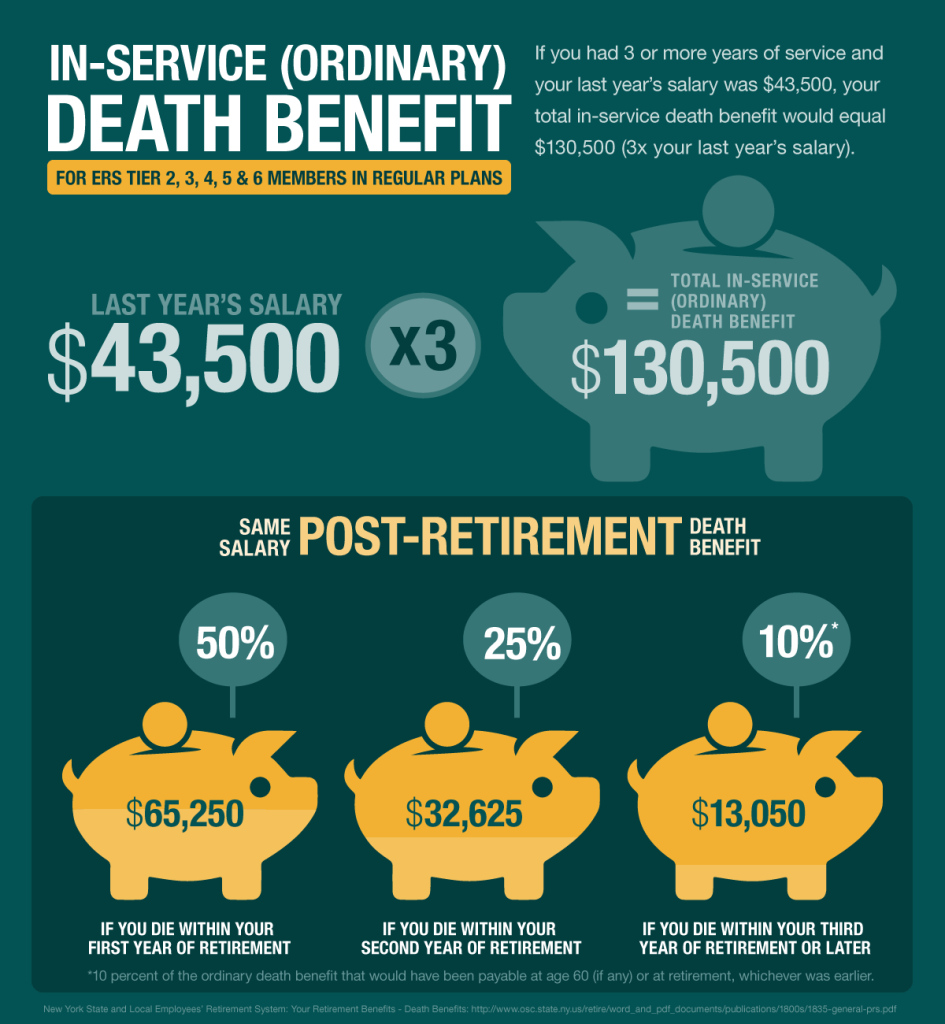

The Ordinary Death Benefit

You’re eligible for the ordinary death benefit when you have one year of service credit. Your beneficiary would receive this benefit if you died while working for a public employer.

- After one year of service, the ordinary death benefit is equal to your last year’s salary.

- After two years of service, the benefit equals two times your last year’s salary.

- After three or more years of service, the benefit equals three times your last year’s salary.

The Post-Retirement Death Benefit

Your beneficiary may also be eligible for a post-retirement death benefit if you retire directly from your employer’s payroll or within one year of leaving covered employment.

- During your first year of retirement, the post-retirement death benefit is 50 percent of your ordinary death benefit payable at retirement.

- During your second year of retirement, the benefit is 25 percent of your ordinary death benefit.

- During your third year and thereafter, the benefit is 10 percent of the ordinary death benefit that would have been payable at age 60 (if any) or at retirement, whichever was earlier.

There may be other death benefits available in your retirement plan. Please read the Death Benefit section in your plan publication for more information. If you have any questions about death benefits, please email us using our secure email form.