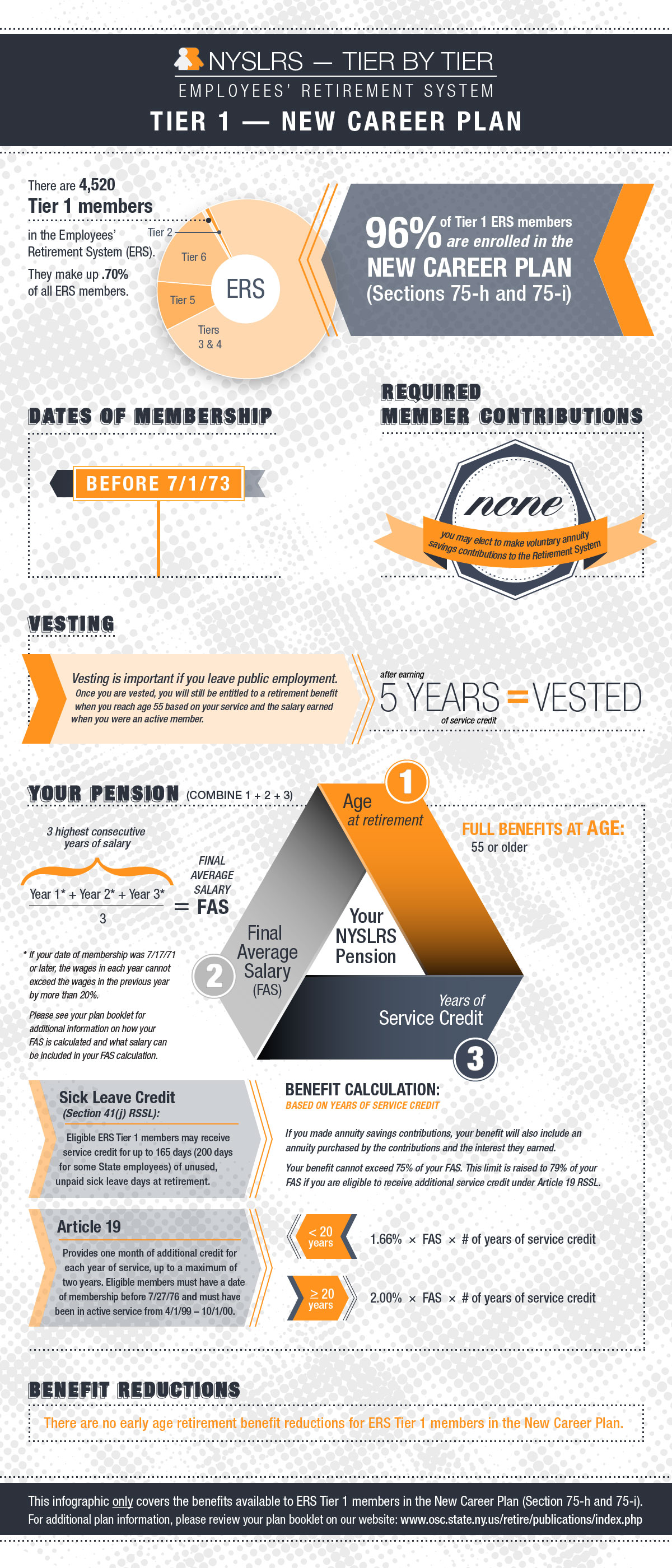

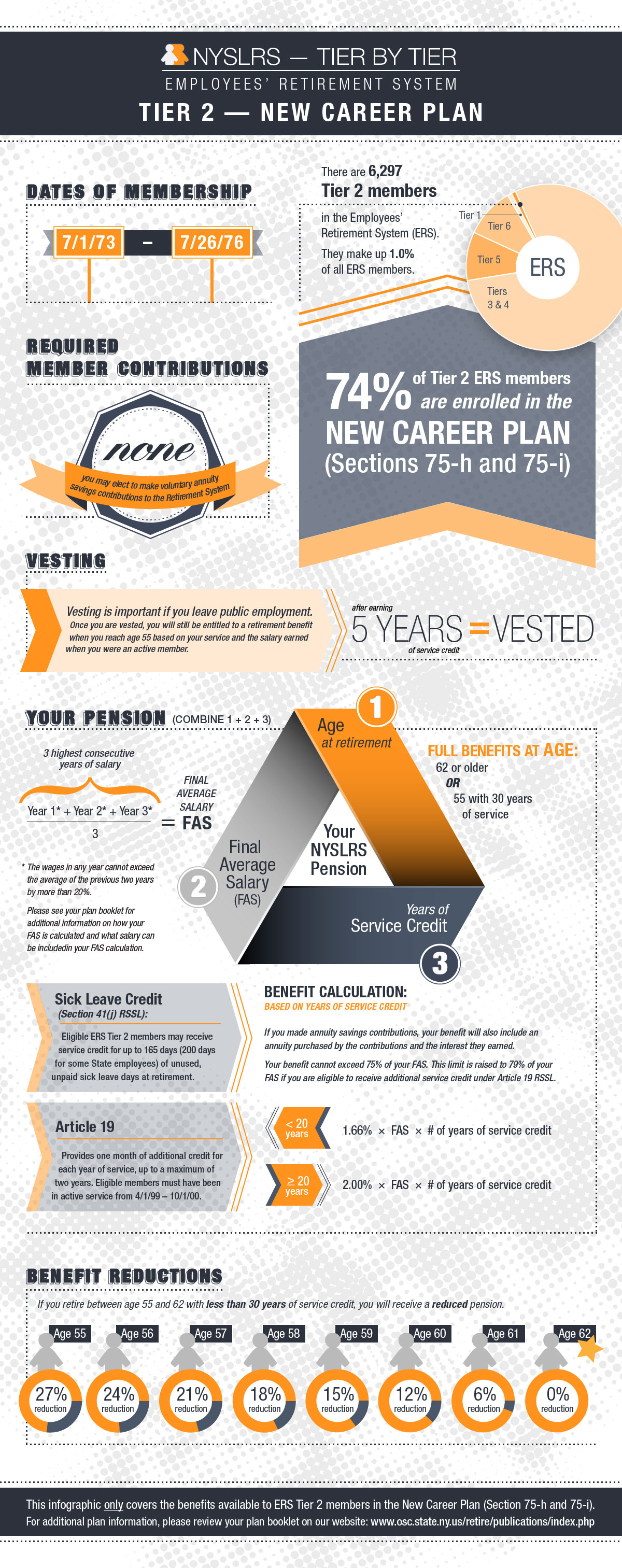

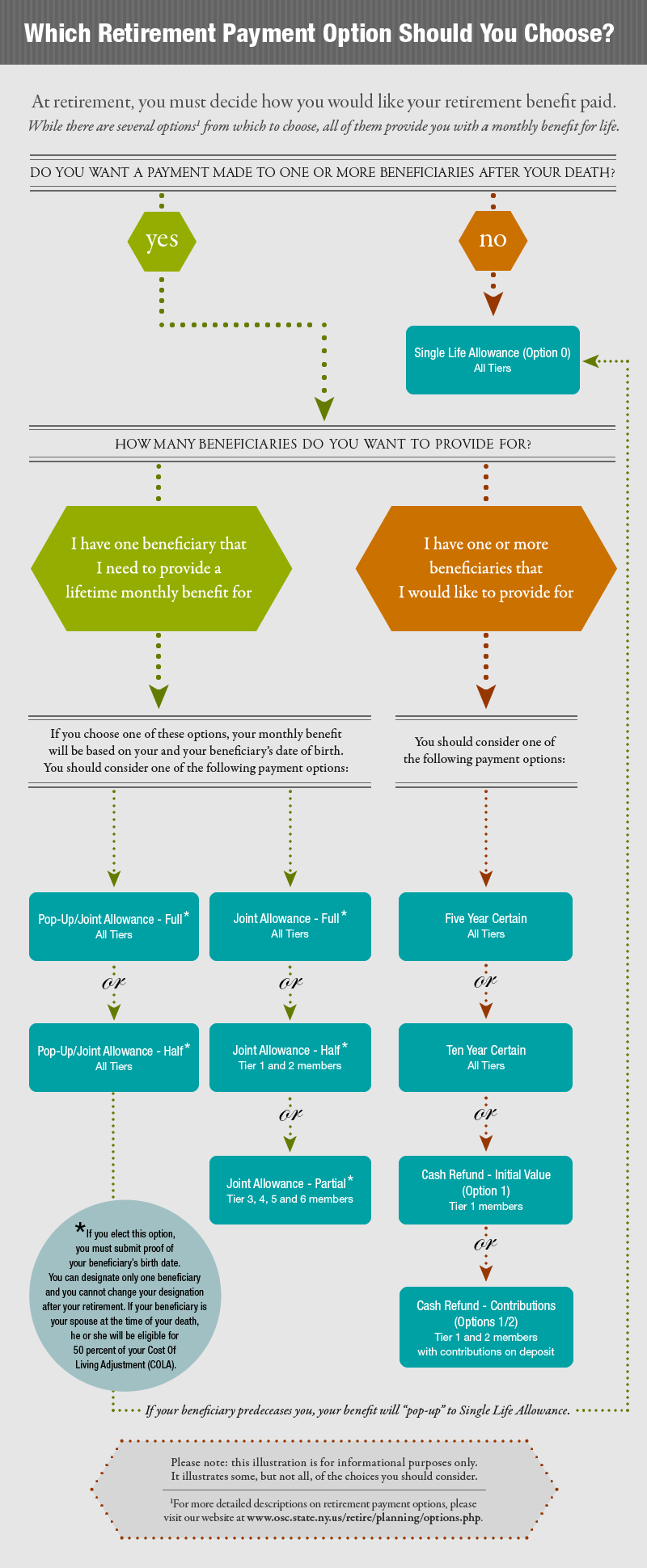

As a NYSLRS member, you have a defined benefit plan that provides a lifetime pension when you retire. Your NYSLRS pension benefit amount will be determined by several factors, including your tier, service credit, and final average earnings (FAE).

When we calculate your pension, we find the consecutive years when your earnings were highest. These are usually your years of employment immediately before retirement, but they can be anytime in your career and do not need to match up with calendar years or fiscal years.

Update: Tier 6 Final Average Earnings Based on Highest Three Years

A new law improves the pension benefits of NYSLRS Tier 6 members. When you retire, your FAE will be based on the average of your three highest consecutive years of earnings, the same as members in other tiers.

These improvements apply to members who retire on or after:

- April 1, 2024, for Police and Fire Retirement System (PFRS) Tier 6.

- April 20, 2024, for Employees’ Retirement System (ERS) Tier 6.

Previously, your FAE was the average of your highest five consecutive years of earnings.

If you recently retired and the change applies to you, we have updated your pension calculation — you don’t need to contact us. The new law does not apply to members who retired before the dates above.

Understanding Final Average Earnings Limits

If your earnings increase significantly through the years used in your FAE, some of those earnings may not be used toward your pension.

Your limit depends on whether you’re an ERS or PFRS member and your tier. For most members, if the earnings in any 12-month period in your FAE exceed the average of the previous two years by more than 10 percent, the amount above 10 percent will not be included in your FAE calculation.

For more information, including limits for other tiers, visit our Final Average Earnings page.

Types of Earnings Included in Your FAE

The specific types of earnings included in your FAE calculation depend on your retirement plan and tier. Please check your plan publication for details.

In most cases, your FAE will include the payments listed below, if they are earned in the FAE period. (In some cases, restrictions may apply.)

- Regular earnings (see earnings limit for Tier 6);

- Overtime earned in the FAE period (see overtime limits for Tier 5 and overtime limits for Tier 6);

- Compensatory overtime;

- Holiday pay; and

- Longevity payments (maximum of one per FAE year), if earned in the years used in the FAE calculation.

In most cases, the following payments will not be included in your FAE calculation:

- Unused sick leave;

- Payments made as a result of working your vacation;

- Any form of termination pay;

- Payments made in anticipation of retirement; and

- Any payments made for time not worked.