This Public Service Recognition Week, we proudly celebrate more than 695,000 members and 470,000 retirees of the New York State and Local Retirement System (NYSLRS) for their service to the people of New York State.

A Brief History of Public Service Recognition Week

This week was created in 1985 to honor those who serve our nation as federal, state, county and local government employees.

Congress officially designated the first full week of May as Public Service Recognition Week. This year, it is being celebrated May 5 through 11.

NYSLRS Members Deliver Critical Services

From the smallest village to our biggest cities, New York public employees like you provide the essential services that improve our quality of life. You work for employers such as:

New York State

Couties, Towns and Villages

School Districts

Correctional Facilities

Public Libraries

Fire and Water Districts

Whether they are protecting public health and safety, driving our children to school or clearing snow from the roads, NYSLRS members deliver the critical services New Yorkers depend on. Many NYSLRS members and retirees also give back to our state by volunteering in their communities or supporting charitable causes.

Comptroller DiNapoli’s Faith in Public Service

New York State Comptroller Thomas P. DiNapoli is the administrator of NYSLRS and trustee of the Common Retirement Fund. His public service career began at 18 years old, when he won his first election to become a trustee on the Mineola Board of Education. That made him the youngest person in New York State history to be elected to public office. He is also the second longest-serving comptroller in New York State history.

Comptroller DiNapoli is understandably proud about the career path he has chosen, and he often speaks about the contributions that New York’s public employees make to their communities and their State. He encourages young people to consider a career in public service. “It’s more than a job,” he says. “It’s a career with purpose.”

Most NYSLRS pensions are subject to federal income tax. If your last federal tax bill or return was larger than you expected and you want to change the amount withheld from your NYSLRS pension, Retirement Online makes it fast and convenient to update your federal tax withholding. If you haven’t signed up yet, learn more about Retirement Online and click “Register Now” to open your account.

Understanding Your Federal Tax Withholding

NYSLRS calculates the amount withheld from your monthly benefit payment based on the information you provide us on a W-4P form (Withholding Certificate for Pension or Annuity Payments).

The Internal Revenue Service (IRS) released a revised version of their W-4P form, which no longer allows tax filers to adjust their withholding by electing a specific number of allowances. To comply with the IRS’ requirements, NYSLRS updated our tax withholding form. You do not need to submit a new W-4P to NYSLRS unless you want to change the amount of your tax withholding.

Updating Your Withholding

Retirement Online provides an online form that collects the same information as the paper W-4P form, and your updates will be made more quickly if you submit them online.

From your Account Homepage, click the green “Update My W-4P Tax Information” button.

Follow the steps to update your withholding.

Basic Withholding

Step 1. Select your filing status. If you want your federal withholding to be based only on the benefit amount you receive from NYSLRS, with no adjustments, you can skip steps 2 – 4.

Adjustments to Withholding (Dependents, Tax Credits)

Complete Steps 2 – 4 ONLY if they apply to you.

Step 2. If you have income from a job or more than one pension/annuity, in addition to your NYSLRS pension, or if you’re married filing jointly and your spouse receives income from a job or pension/annuity, you can enter that in Step 2.

If you update your federal withholding online by the middle of the month, your changes will generally be applied that month. We’ll notify you by mail or email (depending on your contact preference) when the update has been completed.

If You Need Help

Our Taxes and Your Pension page has additional information about federal withholding, including what to do if you receive more than one benefit payment from NYSLRS, 1099-R tax form information and more.

If you need assistance completing the form, visit the IRS’ website and read the current revision of the IRS Form W-4P (detailed instructions start on page 2). You can also find phone numbers and online resources on the IRS’ Let Us Help You page.

If you’re not sure whether you need to adjust your federal withholding or if you have other tax questions, you may want to check with a tax preparer.

As a NYSLRS retiree, you can work and still receive your pension, but you should be aware there may be a limit on how much you can earn each year without affecting your NYSLRS pension.

Working While Receiving a Service Retirement Benefit

An earnings limit of $35,000 generally applies to NYSLRS retirees who:

Are under age 65;

Receive a service retirement benefit (see disability benefit rules below); and

Return to work for a public employer (including contract or consultant work, if you joined NYSLRS on or after May 31, 1973).

2024 Update Regarding the Earnings Limit

The earnings limit for retirees employed by school districts and Boards of Cooperative Educational Services (BOCES) is suspended through June 30, 2025 (April 2024 legislation extended the date from 2024 to 2025). The earnings limit suspension for school employees does not apply to retirees who work for a college, university or charter school.

For most other retirees under the age of 65, the $35,000 limit is in effect and applies to the entire calendar year in 2024.

There is no earnings limit if you are self-employed or if you work for:

The federal government;

A state or local government in another state; or

A private employer.

Also, beginning in the calendar year you turn 65, the earnings limit no longer applies.

Working While Receiving a Disability Retirement Benefit

Almost all earnings for retirees who are working while receiving a disability retirement benefit are limited whether they work for a public or private employer. The limit is specific to each retiree. To find out your earnings limit, please contact us.

How the Limit Applies

The limit applies to all earnings for the calendar year, including money earned in the calendar year, but paid in a different calendar year (for example earned in December but paid in January).

The limit does not apply to:

Payments received after you retire from your employer, such as for vacation or sick time you earned when you were still working; and/or

A retroactive payment for a new union contract, if the earnings are for employment before you retired.

Reporting Your Earnings

It is your responsibility to notify NYSLRS if you earn more than the limit. If you know you are going to exceed the limit, contact us at least a month before you do.

You can message us using the secure contact form, or you can fax a letter to 518-402-2498. Be sure to include the name of your employer, the approximate date you expect to exceed the limit and a daytime phone number in case we have questions.

If You Exceed the Earnings Limit

If you earn more than the limit, you must:

Pay back NYSLRS for the pension payments you received after the date you reached the limit. If you continue to work, your pension will be suspended for the remainder of the calendar year and resume the following January.

OR

Rejoin NYSLRS, in which case your pension will be suspended until you retire again at some future date. (You’d need to reapply.)

Earnings Limit Waiver

Under Section 211 of the Retirement and Social Security Law, the earnings limit can be waived if your prospective employer gets approval before hiring you. Approval is not automatic; it is based on the employer’s needs and your qualifications. In most cases, the New York State Department of Civil Service would be the approving agency. A Section 211 waiver covers a fixed period, normally up to two years.

For More Information

Before you decide to return to work, please read our publication What If I Work After Retirement? It includes information such as how earnings limits are calculated for retirees receiving a disability retirement benefit, consequences to consider before returning to NYSLRS membership and more. If you have questions, please contact us.

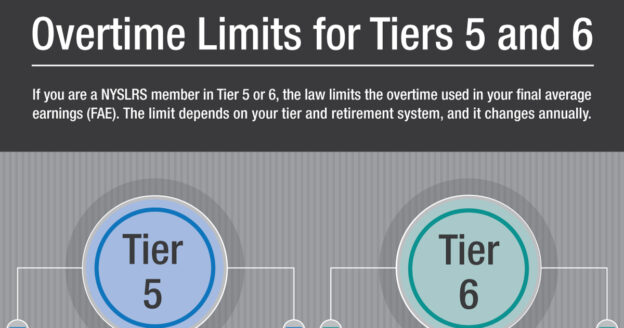

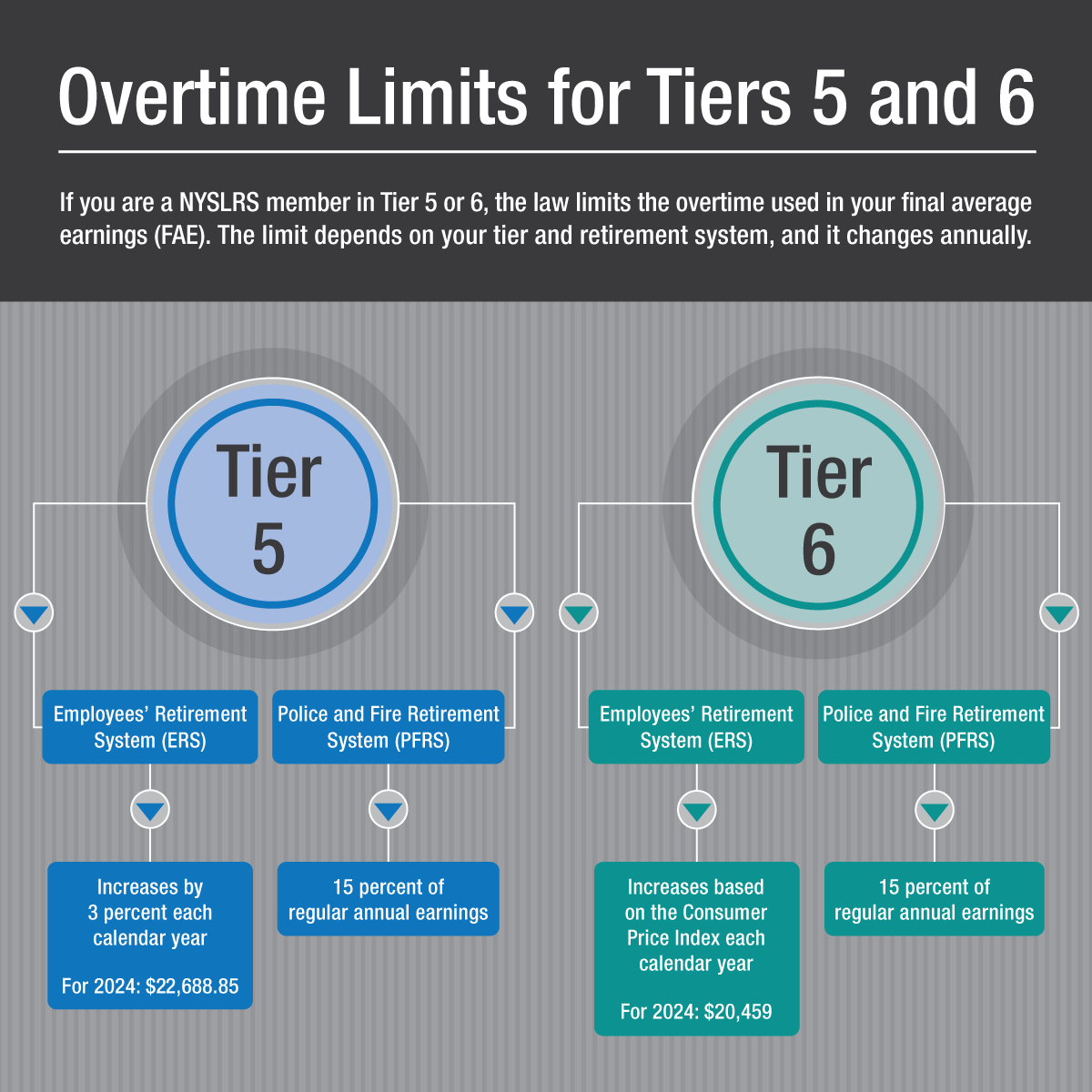

Tier 5 and 6 members are subject to limits on the amount of overtime that can be included in their pension. You can earn overtime pay beyond the overtime limit, but it won’t be factored into your pension calculation. And you don’t pay member contributions on overtime pay that is above the limit.

Tier 5 Overtime Limits

The overtime limit for Tier 5 Employees’ Retirement System (ERS) members increases each calendar year by 3 percent. In 2024, the limit for Tier 5 ERS members is $22,688.85.

For Tier 5 Police and Fire Retirement System (PFRS) members, the overtime limit is 15 percent of your regular earnings each calendar year.

The overtime limit for Tier 6 ERS members increases each calendar year based on the annual increase of the Consumer Price Index (CPI). In 2024, the limit for Tier 6 ERS members is $20,459.

For Tier 6 PFRS members, the overtime limit is 15 percent of your regular earnings each calendar year.

Your NYSLRS pension will be based on your service credit and final average earnings (FAE). Your FAE is the average annual earnings you receive during the period when your earnings are highest (36 consecutive months for Tier 5 and 60 consecutive months for Tier 6). Your FAE will include overtime pay you earned up to each annual limit.

Your FAE may be limited in other ways. For example, for most members, if your earnings increase significantly in the years used for your FAE, some of those earnings might not count toward your pension. The specific limits depend on your tier. Visit our Final Average Earnings page for more information about this limit.

Your retirement plan publication provides specific information about the earnings that will be used to calculate your pension. Visit our website to Find Your NYSLRS Retirement Plan Publication.

Estimate Your Pension in Retirement Online

Most members can create their own pension estimate in minutes using Retirement Online. You can enter different retirement dates to see how those choices would affect your benefit. Sign in to Retirement Online and click the “Estimate my Pension Benefit” button to try it.

Planning on taking out a NYSLRS loan? Applying through Retirement Online is fast and convenient.

Eligibility for a NYSLRS loan is based on your tier. Generally, you’ll need to be on the payroll of a participating employer, have at least one year of service and have sufficient contributions in your account. (Note: Retirees are not eligible for NYSLRS loans.)

Retirement Online is the Fastest Way to Apply

When you use Retirement Online, NYSLRS receives your application immediately and can process your loan more quickly. It’s also an easy way to check the amount you are eligible to borrow, your balance on any outstanding loans, and more.

In the ‘I want to…’ section, click the “Apply for a Loan” button.

Follow the prompts.

As you work your way through the online application, you’ll see:

How much you are eligible to borrow;

The minimum repayment amount;

The expected payoff date; and

How much you can borrow without tax implications.

If you apply for a loan and you already have an existing loan (or loans), you’ll choose one of two options:

Multiple loans: With multiple loans, you are taking a new loan, and each of your outstanding loans has a separate five-year due date and minimum payment. The minimum payments for each of your loans are added together for one total minimum payment. This combined minimum payment amount is higher than the minimum would be if you choose a refinanced loan, but with multiple loans, as each loan is paid off, your total minimum payment goes down.

Refinance your existing loan: Refinancing your loan adds your new loan amount to your existing balance and consolidates the entire amount as one loan instead of taking separate loans. Minimum payment amounts for refinanced loans are lower than the minimum for multiple loans because when you refinance, we combine your existing loan balance with your new loan and spread out the repayment over a new five-year term. However, this increases the portion of your loan that may be considered a taxable distribution, and federal withholding can significantly reduce the loan amount that you receive.

There is a service charge of $45 that will be deducted from your loan check when it is issued. The current interest rate is 5 percent. The interest rate will remain fixed for the term of your loan.

If your case status says “Closed” before close of business on Wednesday, your check will be in the mail that Friday.

You will also receive a confirmation letter when your loan case has been completed. You can find it in your Retirement Online account under “View Documents.”

Repaying Your NYSLRS Loan

Loan payments are deducted from your paycheck. If you choose to repay the minimum amount, your payroll deduction may be increased periodically to ensure your loan will be repaid within the required five-year repayment term. You can increase your payroll deduction amount, make additional payments or pay your loan in full at any time with no prepayment penalties. Retirement Online is the easiest way to manage your loan payments. Sign in to your account and select “Manage my Loans.”

Retiring With an Outstanding NYSLRS Loan

If you retire with an outstanding loan, your pension will be reduced. You will also need to report at least a portion of the loan balance as ordinary income (subject to federal income tax) to the IRS. If you retire before age 59½, the IRS may charge an additional 10 percent penalty. If you are nearing retirement, be sure to check your loan balance. If you are not on track to repay your loan before you retire, you can increase your loan payments, make additional lump sum payments or both in Retirement Online.

Note: Employees’ Retirement System (ERS) members may repay their loan after retiring, but they must pay the full amount (that is, the amount that was due on their retirement date) in a single lump-sum payment. Once you do, your pension benefit will increase from that point on, but it will not be adjusted retroactively back to your date of retirement.

Visit Our Website for More Information

For more information about NYSLRS loans, including what happens if you go off payroll or default on your loan, visit our Loans page. Need help with Retirement Online? See our Tools and Tips blog post.

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. If you are retired, your beneficiaries may be entitled to a post-retirement death benefit.

It’s important to name beneficiaries and review them periodically. Life circumstances sometimes change, and the beneficiary you named before might not be the one you would choose today. For example, if you just married, you may want to update your NYSLRS account information to name your new spouse as your beneficiary.

2 Types of Beneficiaries

Your primary beneficiary will receive your death benefit. You can list more than one primary beneficiary. If you do, they will share the benefit equally. Or you can choose different percentages for each beneficiary to total 100 percent. (Example: John Doe, 50 percent; Jane Doe, 25 percent; and Mary Doe, 25 percent.)

A contingent beneficiary will only receive a benefit if all your primary beneficiaries die before you do. If you list multiple contingent beneficiaries, they will share the benefit equally unless you choose different percentages.

Special Beneficiary Designations

Your beneficiary doesn’t have to be a person. You can name a charity, a trust or your estate as your beneficiary.

Estate. When you die, your estate is the money and property you owned. Your death benefit will be given to the executor of your estate to be distributed according to the terms of your will. You can name your estate as the primary or contingent beneficiary of your death benefit. If you name your estate as the primary beneficiary, do not name a contingent beneficiary.

Trust. You can name a trust as a primary or contingent beneficiary if you have a trust agreement or provided for a trust in your will. The trust itself would be your beneficiary, not the individuals for whom you established the trust. (Speak with your attorney if you’re thinking about making your trust a beneficiary.)

Entity. You can also name any charitable, civic, religious, educational or health-related organization as a beneficiary.

Minor children. If your beneficiary is under the age of 18 at the time of your death, your benefit will be paid to the child’s court-appointed guardian. You may instead choose a custodian to receive the benefit on the child’s behalf under the Uniform Transfers to Minors Act (UTMA). Custodians can be designated in Retirement Online or you can contact us for more information and the appropriate form before making this type of designation.

Keep Your Beneficiaries Up to Date

You can change your beneficiaries at any time. In addition to adding or removing them to reflect your current wishes, you should review the contact information for your named beneficiaries so we can find them when needed.

The fastest way to view or update your beneficiaries is in Retirement Online.

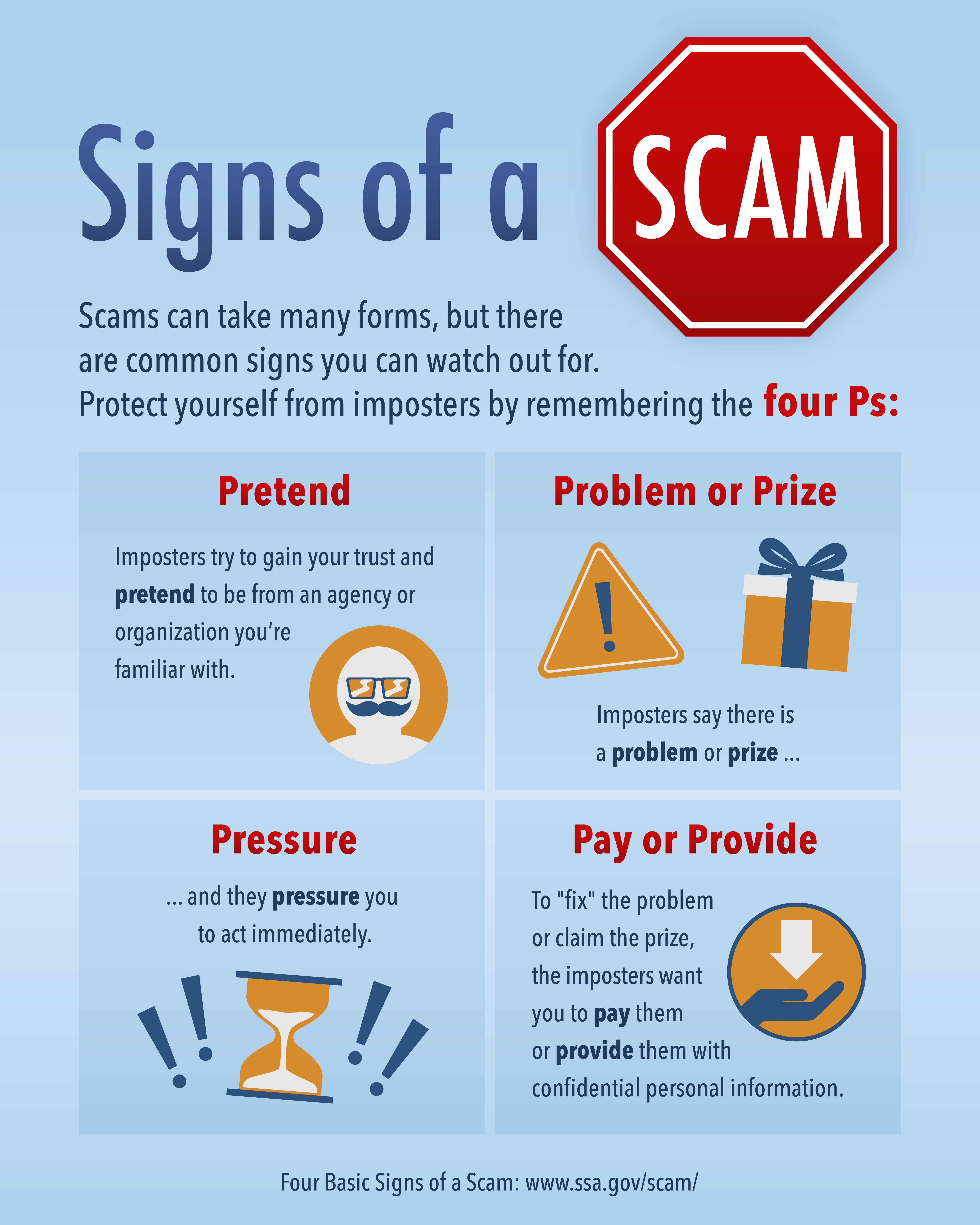

Your retirement account can be an attractive target for scammers, and imposters continue to find new ways to try to impersonate government agencies, such as NYSLRS or the Social Security Administration. Learn to distinguish fake messages from official NYSLRS communications and protect yourself from scams.

How Scams Work

Imposters pretend to be an agency or organization you already know to gain your trust. They use similar logos or imagery in correspondence. They may contact you from an email address that mimics — but isn’t identical to — those used by employees of the actual organization. Some can even make a real agency’s phone number appear on caller ID (known as spoofing).

Usually, once they contact you, they claim there is a problem (or prize or new benefit available) that requires your immediate attention. But here’s the catch: to fix the problem or receive the reward, the imposter needs you to pay them a fee or provide personal data, such as your Social Security number or bank account information. They may even threaten you with legal action, a suspension of your benefits or arrest if you fail to act in time.

If someone contacts you and you notice these signs of a scam, remain calm. Hang up the phone or delete the message if you feel like something is off. It’s the easiest way to avoid accidentally giving away personal information.

Artificial Intelligence Gives Scammers a New Tool

You should also be aware of an emerging threat — artificial intelligence (AI), which allows machines to mimic certain human behaviors, such as speech and writing. AI can personalize phishing emails, making it harder to recognize a fraudulent communication. It can impersonate the voice of a family member or friend, making you think they are in trouble or need money.

Here are some things you can do to protect yourself from AI-enhanced scams:

Don’t share sensitive information through text or social media;

Don’t send or transfer money to unknown locations;

Consider designating a “safe word” for your family to use to identify themselves and share that word with family members and close contacts; and

When in doubt, hang up and call your loved one back.

Doing Business With NYSLRS

Retirement Online, the convenient and secure way to do business with NYSLRS, is only available from the NYSLRS website. There is no mobile app available from NYSLRS. If you have a Retirement Online account, keep your username and password in a safe place and don’t share them with anyone.

Generally, NYSLRS will only call you if we are following up on a previous communication from you, such as a phone call, secure email message, Retirement Online request, form or letter. For security, you can use your NYSLRS ID to identify yourself instead of providing your Social Security number. To find your NYSLRS ID, sign in to Retirement Online, or check your annual statement or other correspondence from NYSLRS.

It’s important to review the communications you receive from NYSLRS. We send you letters or emails (depending on your delivery preference in Retirement Online) whenever you update your Retirement Online account or benefit information. However, if you receive a notification of an account change you did not make, contact us immediately.

Keep Your Password Current

Also, be sure to sign in to Retirement Online at least once a year and update your password so it doesn’t expire.

Your Retiree Annual Statement is now available in Retirement Online! Retirees who opted to go paperless already received an email notifying them that their Statement is available in their Retirement Online account.

If you did not change your delivery preference to email, your Statement will be mailed by the end of February.

Get Your Statement Online Now

Whether you chose email delivery or not, you can access your Statement in your Retirement Online account now. To view, save or print your Statement:

From your Account Homepage, click the “View My Retiree Annual Statement” button.

Follow the prompts.

If you don’t have an account, you can find step-by-step instructions for registering in the Tools & Tips section of the Retirement Online page.

Inside Your Retiree Annual Statement

Your Statement has a new look this year, but it still contains the same information you receive every year about your benefit amount, deductions and tax withholding. Your Retiree Annual Statement includes:

Your NYSLRS ID. To protect your privacy, use this number instead of your Social Security number when conducting business with NYSLRS.

The total amount of your annual benefit. (This is your base benefit, before taxes, deductions and credits.)

Your total net benefit for the year. (This is your benefit after taxes, deductions and credits.)

Other deductions taken from your pension, such as payments to an alternate payee or union dues.

Health insurance premiums. (NYSLRS doesn’t administer health insurance benefits, but we deduct retiree premiums at the request of your former employer.)

Next Year Don’t Wait for the Mail

Going forward, your Statement will be available online in early February each year.

Update your delivery preference now to receive an email as soon as next year’s Retiree Annual Statement is available online:

From your Account Homepage, click the “update” link next to ‘Retiree Annual Statement by.’

Choose “Email” from the dropdown.

If you choose to receive your Statement by email, you will not receive a printed copy in the mail.

Use Retirement Online to Stay Informed

Your Statement is a snapshot of your NYSLRS account as of December 31, 2023. For the most up-to-date information year-round, sign in to Retirement Online. If you don’t already have an account, you can learn more or register today.

In Retirement Online, you can view pay stubs for your benefit payments. Check them if you have a question or to track year-to-date totals of your pension benefit as well as any deductions for health insurance, union dues, tax withholding or disbursements under a domestic relations order.

Your Statement is Not a Tax Document

While your Retiree Annual Statement does include information about your benefit payments and tax withholding, it is not a tax document. If your pension is taxable, you should have received a 1099-R tax form (either through your Retirement Online account or by mail, depending on your delivery preference) for filing your taxes.

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.

Most NYSLRS pensions are subject to federal income tax (some disability benefits are not taxable). If you receive taxable income from NYSLRS, we provide a 1099-R tax form for filing your taxes. New this year, retirees who opted to go paperless received an email notifying them their 1099-R is available in their Retirement Online account. If you did not change your delivery preference to email, your 1099-R tax form will be mailed to you by January 31.

Understanding Your 1099-R

A 1099-R tax form is used to report the distribution of taxable retirement benefits. It shows:

The total benefit paid to you in a calendar year.

The taxable amount of your benefit.

The amount of taxes withheld from your benefit.

If you have questions about the information on the form, check our interactive 1099-R tutorial. It walks you through a sample 1099-R and offers a short explanation of each box on the form.

Get Your 1099-R Online Now

Whether you chose email delivery or not, you can access your 1099-R in your Retirement Online account now. To view, save or print your 1099-R:

Your NYSLRS pension can provide a significant portion of your retirement income, but it’s also a good idea to supplement your pension and Social Security with a retirement savings account.

Retirement savings can be an important financial asset when you retire. Savings can enhance your retirement lifestyle and give you the flexibility to do the things you want. Your savings can provide money for you to travel, continue your education, pursue a hobby or start a business. The money you set aside can also be a resource in case of an emergency, act as a hedge against inflation and boost your retirement confidence.

Set a Retirement Savings Goal

How much to save is a personal decision, but here are some things to consider.

Financial advisers often recommend saving 10 to 15 percent of your gross earnings throughout your career to retire comfortably. However, that advice is aimed at people with 401(k)-style defined contribution retirement plans as their main source of retirement income.

As a NYSLRS member, you’re part of a defined benefit plan, also known as a traditional pension plan. Your pension, based on your years of service and earnings, will provide a lifetime benefit. You can estimate your pension in Retirement Online to get an idea of the income it will provide in retirement.

Having a pension means you may not need to save as much as someone with only a 401(k). Use a retirement savings calculator to see how much a retirement savings plan could yield over time, or test the results of different savings amounts.

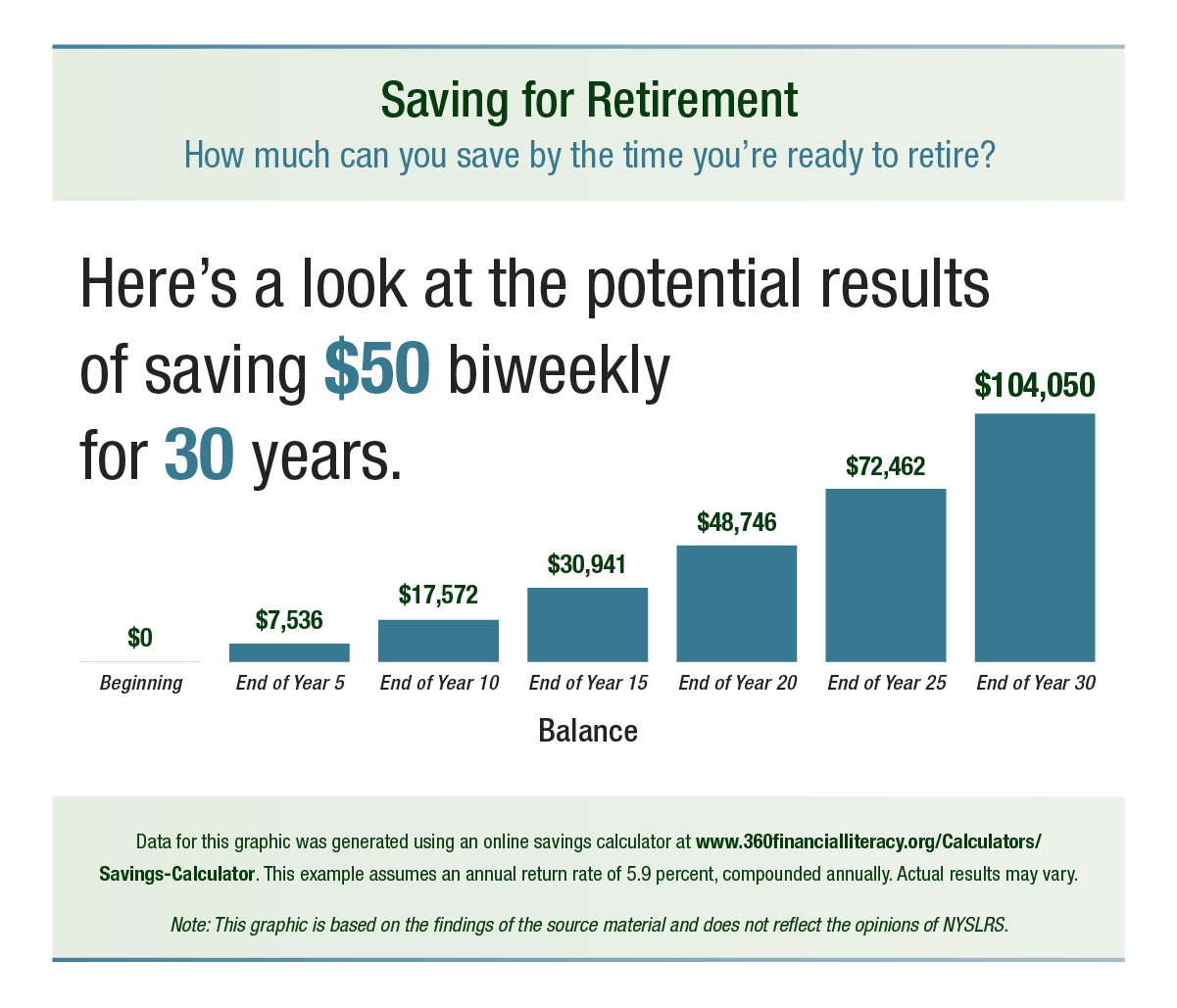

Below you can see potential savings results of someone who invests 50 dollars every two weeks over 30 years. While the stock market can be turbulent over the long term, stock market returns average about 10 percent a year.

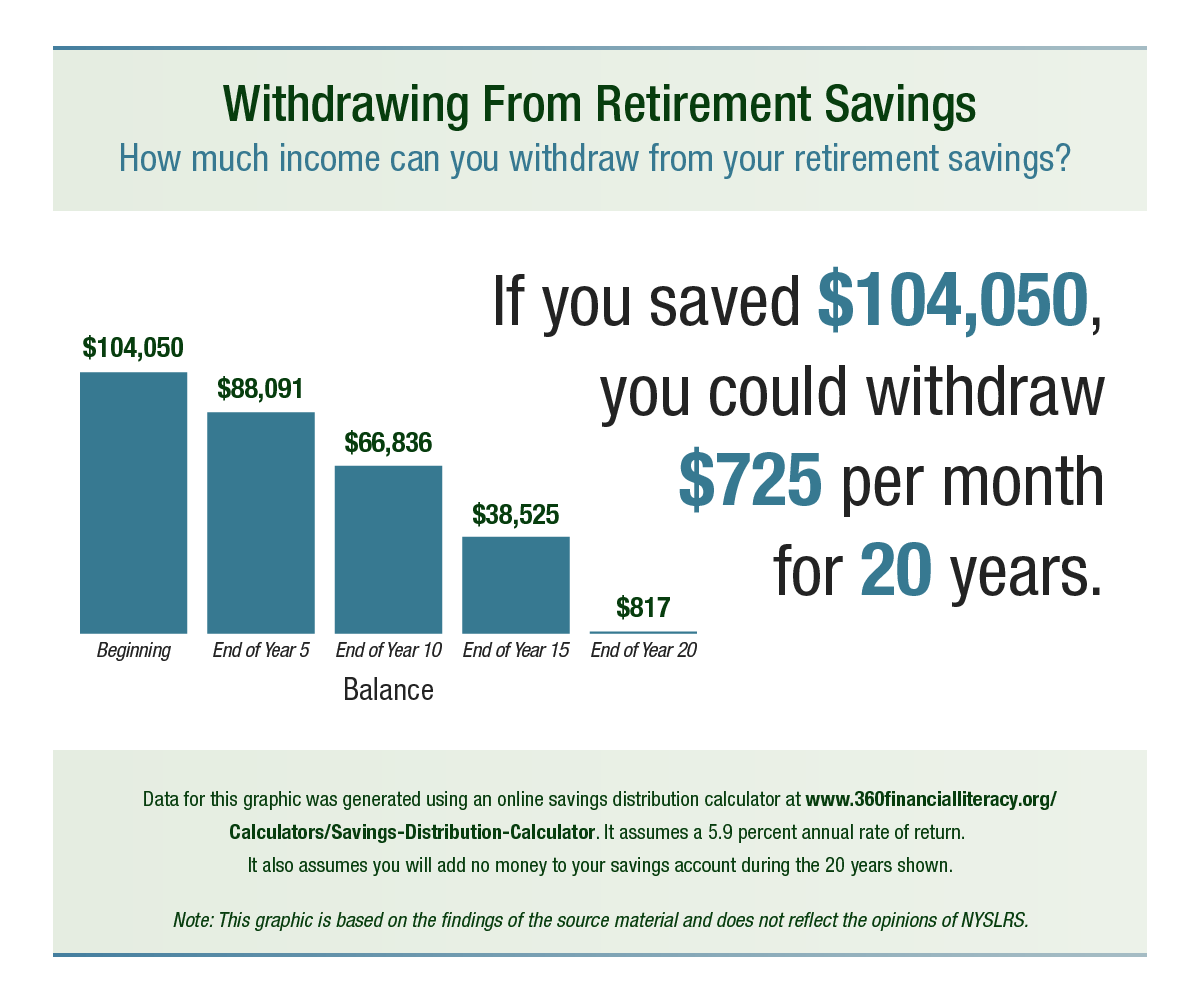

As you get closer to retirement, you should develop a plan to withdraw money from your retirement savings. A withdrawal plan will give you a better idea of the income you might expect from your nest egg.

Here is one possible withdrawal strategy, which was designed to provide retirement income for 20 years. Please note, if your retirement is far in the future, the money you withdraw may not have the same value that it has today. However, while inflation has been high recently, it does cycle and has been lower in the past.

If you find you’ll need to save more to meet your goal, you can make adjustments to help ensure you’ll have enough savings in retirement.

Deferred Compensation – A Way to Save

State employees and many municipal employees are eligible to save for retirement through the New York State Deferred Compensation Plan. Once you’ve signed up, your retirement savings, which may be tax-deferred, depending on your plan, will be automatically deducted from your paycheck. (The Deferred Compensation Plan is not affiliated with NYSLRS.)

Check with your employer’s human resources or personnel office to see if they participate in the Deferred Compensation Plan or if they offer other savings options.

Read More About Retirement Savings

You can find more information about saving for retirement in these posts:

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.

Tax season is approaching, and with 1099-Rs available online, getting this key NYSLRS tax form is now faster and more convenient than ever.