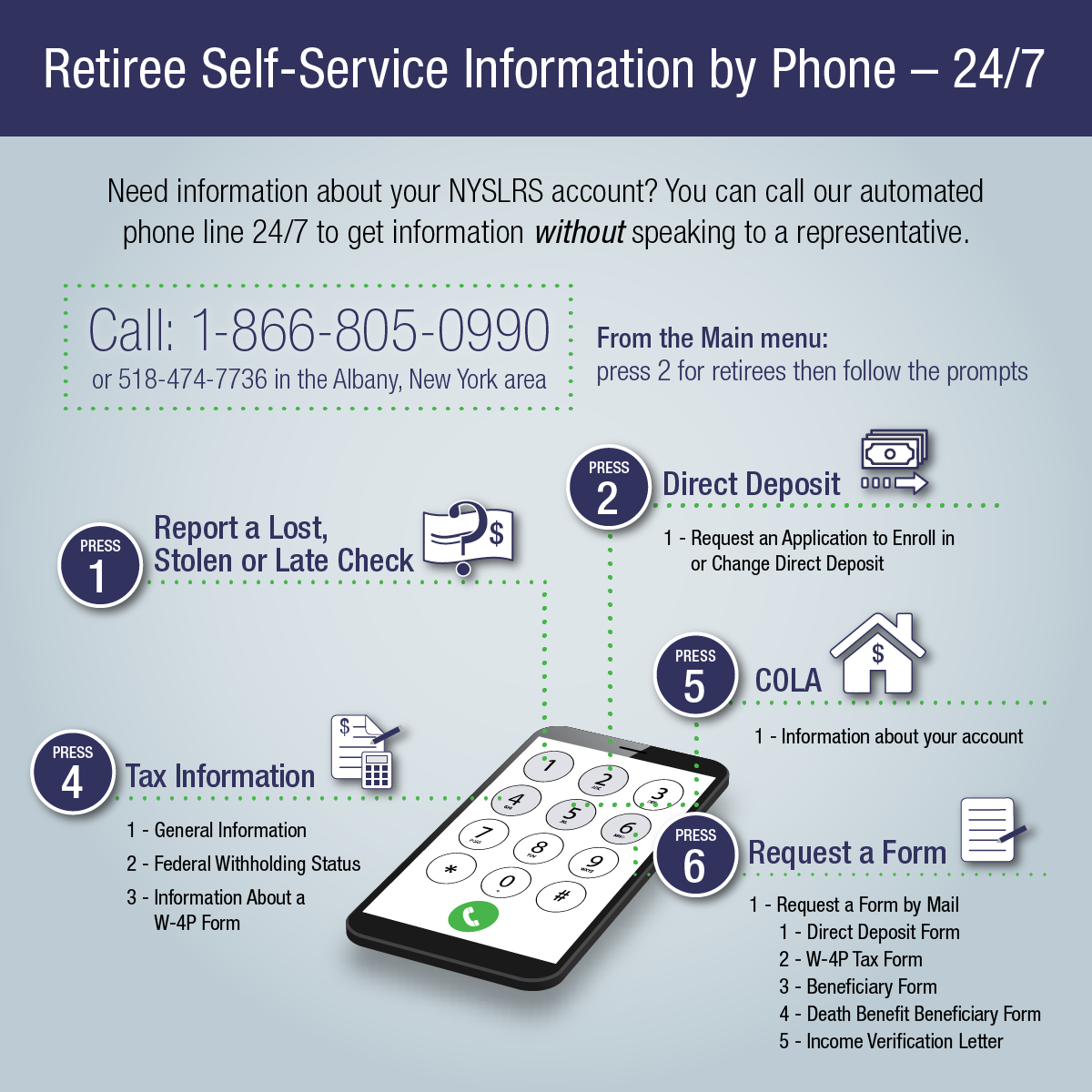

Under normal circumstances, NYSLRS won’t release your benefit information – even to close family members – without your permission. However, if we have an approved copy of your power of attorney (POA) form on record, we can discuss your information with the person you named as your agent in your POA.

For example, your agent could ask for details about your pension payments, get help completing a loan application or call us for clarification if you don’t understand a letter you received.

Your agent could be your spouse, another family member or a trusted friend. You may designate more than one person as your agent, and you may authorize those agents to act together or separately. You may also designate “successor agents” to act on your behalf if the primary agent is unable or unwilling to serve.

A POA form may be filed with NYSLRS at any time, so there’s no need to wait until a “life event” happens to file. With a POA already on record, the designated agent can act immediately in case of emergency, hospitalization or unexpected illness.

What Can Agents Do?

The agent named in your POA is authorized to act on your behalf and conduct business with NYSLRS for you.

Agents can file applications and forms, such as service or disability retirement applications. They can get account-specific benefit information, request copies of retirement documents, update addresses and phone numbers, and take out loans. For retirees, agents can change the amount withheld from your pension for taxes.

The NYSLRS POA Form

NYSLRS provides a Special Durable Power of Attorney form that is specific to retirement transactions and meets all New York State legal requirements.

If you use the NYSLRS POA form, and your agent or successor agent is your spouse, domestic partner, parent or child, they have “self-gifting authority.” That means they can designate themselves as a beneficiary of your pension benefits or, if you are not yet retired, choose a retirement payment option that provides for a beneficiary after your death and designate themselves as a beneficiary for that benefit.

If your agent or successor agent is not your spouse, domestic partner, parent or child, they do not automatically have self-gifting authority. If you want them to be able to designate themselves as beneficiaries, you should indicate that in the Modifications section of the POA. You should identify your agent by name and specify the authority you want granted to them.

It’s important to note that the NYSLRS POA form only covers Retirement System transactions. It does not authorize an agent to make health care decisions or changes to a Deferred Compensation plan.

Changes to the POA Law

The law governing POA requirements was changed effective June 13, 2021. Any POA executed on or after that date must comply with the following requirements (the NYSLRS form complies with the requirements):

- All POAs must be signed by two disinterested witnesses (witnesses who are not listed as an agent in the POA or named in the POA as a person who can receive gifts).

- The use of a Statutory Gift Rider to grant gifting authority has been eliminated. If you do not use the NYSLRS POA form and instead submit a separately prepared Statutory POA form, gifting authority, even for a close family member, must be granted in the Modifications section of the POA. (See our Power of Attorney page for details.)

If you have an approved POA on file with NYSLRS, you do not need to send a new one. POAs executed before June 13, 2021, will be reviewed in accordance with the laws in effect at the time. POAs executed on or after June 13, 2021, that use an old POA form or do not comply with other requirements of the new law will not be valid.

How to Submit a POA Form

You can scan and email a copy of your POA to NYSLRS using our secure email form.

You can also mail your POA (original or photocopy). You may wish to mail it certified mail, return-receipt requested, so you know when NYSLRS receives it. Mail it to:

NYSLRS

110 State Street

Albany, NY 12244-0001.

Find Out More

A power of attorney is a powerful document. Once you appoint someone, that person may act on your behalf with or without your consent. We strongly urge you to consult an attorney before you execute this document.

You may revoke your POA at any time by sending us a signed, notarized statement.

Please read the Power of Attorney page on our website for additional information.