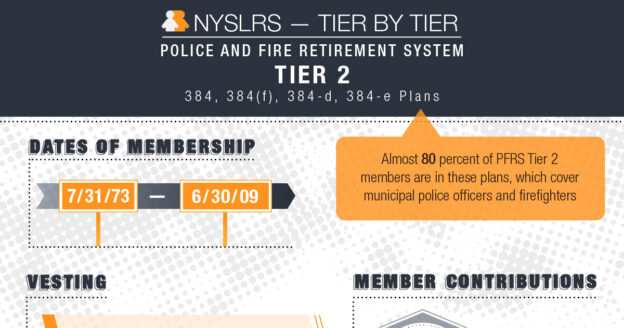

When you join the New York State and Local Retirement System (NYSLRS), you’re assigned a tier based on the date of your membership. This post looks at Tier 2 members of the Police and Fire Retirement System (PFRS).

Your tier determines such things as your eligibility for benefits, the calculation of those benefits, death benefit coverage and whether you need to contribute toward your benefits.

PFRS has five tiers. Almost half of PFRS members are in Tier 2, which began on July 31, 1973, and ended on June 30, 2009. Most are in special retirement plans that allow for retirement after 20 or 25 years, regardless of age, without penalty.

The special plans that cover most police officers and firefighters fall under Sections 384, 384(f), 384-d, and 384-e of Retirement and Social Security Law. You can sign in to Retirement Online to find your benefit plan, which is listed under ‘My Account Summary.’

Where to Find PFRS Tier 2 Information

Whether you’re in one of the retirement plans described in this post or another retirement plan, we encourage you to visit our website to find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits you’re entitled to receive as a PFRS member.

You can check your service credit total and estimate your pension using Retirement Online. Most members can use our online pension calculator to create an estimate based on the salary and service information NYSLRS has on file for them. You can enter different retirement dates to see how your choices would affect your potential benefit.

Members may not be able to use the Retirement Online calculator in certain circumstances, for example, if they have recently transferred a membership to NYSLRS, if they are a Tier 6 member with between five and ten years of service, or if they have worked for multiple employers and were covered by different retirement plans. These members can contact us to request an estimate or use the “Quick Calculator” on our website. The Quick Calculator generates estimates based on information you provide.

NYSLRS membership provides more than just retirement benefits. For most members, if you die while in active service, your beneficiary may be eligible to receive a death benefit. Here is an overview of member death benefits. If you are retired, visit our Death Benefit page for retirees to learn about your available benefits.

Types of Death Benefits

Most members who die while they’re still working will leave their beneficiaries what’s called an “ordinary death benefit.” This is a lump sum payment that’s usually equal to one year of your earnings per year of service, up to a maximum of three years.

Generally, to leave your beneficiaries this death benefit, you must have at least one year of service credit and your death must occur while you are on the public payroll.

Some members who die because of an on-the-job accident (not due to their own willful negligence) may leave their beneficiary an accidental death benefit. The accidental death benefit is a pension payable to your spouse. Other beneficiaries, as specified by law, may be eligible if there is no spouse.

For Employees’ Retirement System (ERS) Tier 4, 5 and 6 members, the benefit would be 50 percent of your earnings from your last year of service.

For most other members, the benefit would be 50 percent of your final average earnings (less any workers’ compensation benefit).

There is no minimum service credit requirement to leave an accidental death benefit.

The specific death benefits that may be available to your beneficiaries depend on your tier and retirement plan. Find Your NYSLRS Retirement Plan Publication and check it for specific benefit amount and eligibility information.

Note: For public employees who contract COVID-19 on the job and die from COVID-19, their beneficiaries may be eligible for an enhanced death benefit. Find out more about the Enhanced Death Benefit for Survivors of COVID-19 Victims.

Review and Update Your Beneficiaries

You should periodically review your beneficiary designations. Life circumstances sometimes change, and the beneficiary you may have named before might not be the one you would choose today. You should also make sure your beneficiary’s contact information is up to date so we can find them when needed.

Retirement Online is the best way to manage your beneficiary information. Sign in to Retirement Online today and click “View and Update My Beneficiaries” to review your named beneficiaries, and update them if needed.

Reporting a Death

NYSLRS cannot pay out death benefits until after we are notified of a member’s death and have a certified copy of the death certificate. The fastest way for survivors to report a member’s death to NYSLRS is using our online form on our website. Survivors can also upload a copy of the certified death certificate, which enables us to start reaching out to the beneficiary. It’s important to talk with your family about your benefits and how to report your death to NYSLRS.

Payment of Death Benefits

NYSLRS will reach out to your beneficiaries on file and send them the application and instructions for receiving benefits. NYSLRS can pay death benefits once it receives the required documentation.

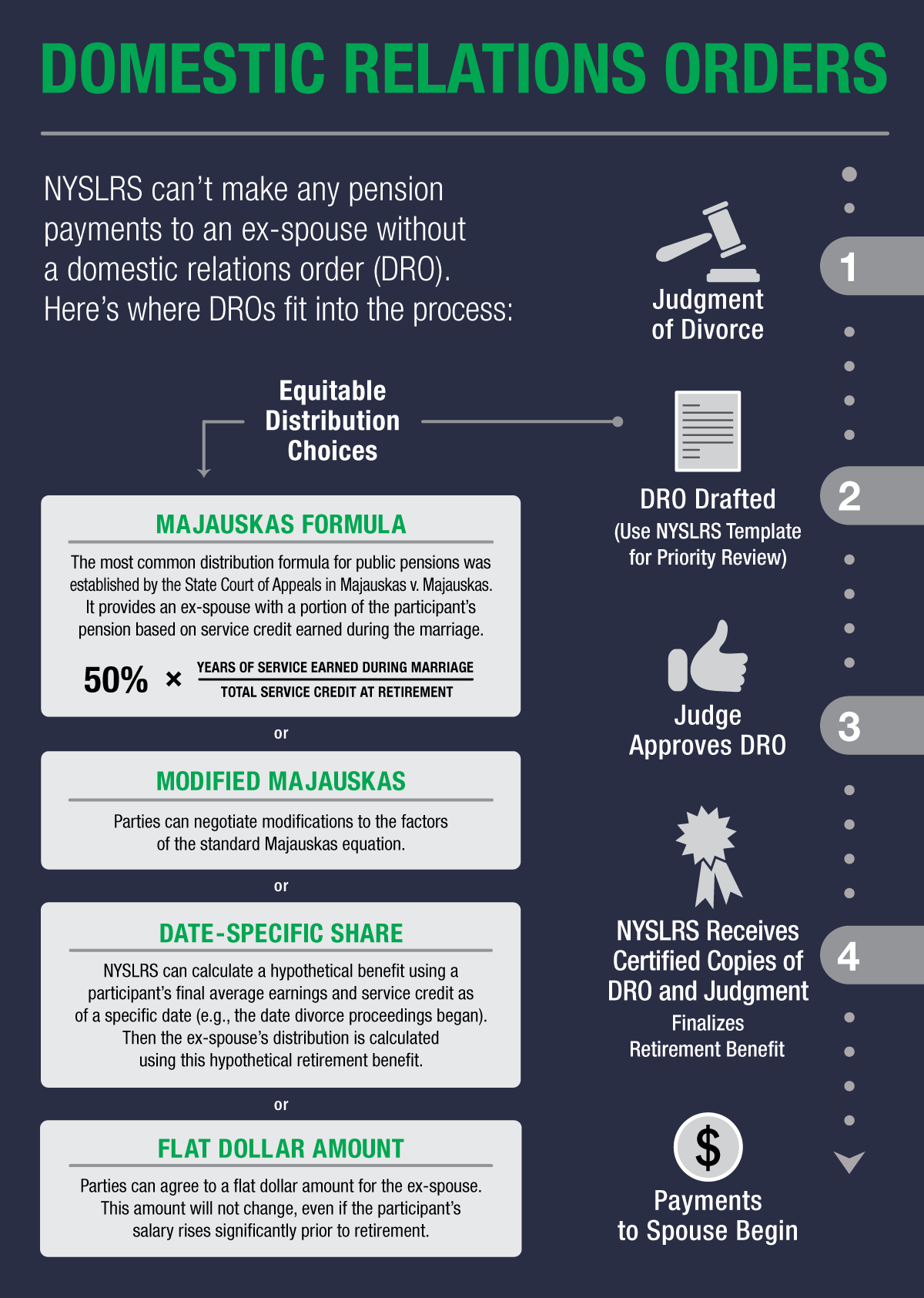

We’ve written before about how divorce may affect your pension benefit. However, NYSLRS members have other benefits besides their pension, and divorce may affect some of them as well.

NYSLRS must have an approved Domestic Relations Order (DRO) on file to pay benefits to the ex-spouse of a member. The DRO is a court order, issued after a final judgment of divorce, that gives NYSLRS specific instructions on how your benefits should be split.

Ordinary Death Benefit

A DRO may direct you to designate your ex-spouse as a beneficiary for some portion of your ordinary death benefit. This is the death benefit that would be payable to your beneficiaries if you die in active service (before retiring) so you should file the DRO with NYSLRS as soon as it’s officially accepted by the court. Be sure to choose additional beneficiaries for any remainder of the benefit and submit your changes to NYSLRS. (If your designations conflict with the terms of the DRO, the DRO will take precedence over any other beneficiary designations.)

Post-Retirement Death Benefit

Most Tier 2, 3, 4, 5 and 6 members of the Employees’ Retirement System (ERS) are covered by a post-retirement death benefit. A DRO may direct you to designate your ex-spouse as a beneficiary for some portion of the benefit.

Accidental Death Benefit

Your accidental death benefit becomes available to specific beneficiaries if you die as a result of an on-the-job accident. Those beneficiaries are designated by law, and only those beneficiaries may receive this benefit — even if there is a DRO.

Loans

NYSLRS members who meet eligibility requirements can borrow a certain percentage of their contribution balance. DROs may be written to prohibit members from taking future loans.

Outstanding loan balances at retirement reduce retirees’ pension benefits. The ex-spouse’s share of the pension will also be reduced unless the DRO specifically provides that the ex-spouse’s share be calculated without reference to outstanding loans.

Contribution Refunds

Occasionally, NYSLRS may refund a member’s contributions because of a tier reinstatement, membership withdrawal or membership transfer. Some members are eligible to make voluntary contributions and withdraw them as excess contributions. Generally, if a DRO doesn’t mention a contribution refund, the member will receive the full amount.

Divorce, Annulments, Separation and Your Beneficiaries

As of July 7, 2008, beneficiary designations for certain death benefits are automatically revoked when a divorce, annulment or judicial separation becomes final. If you are divorced, it is especially important to review your beneficiary designations to ensure your benefits will be distributed according to your wishes and your divorce agreement.

The best way to view and update your death benefit beneficiaries is by using Retirement Online. You can also submit a paper designation of beneficiary form. Visit our View and Update Your Beneficiaries page for more information and instructions. If you are already retired, visit our Death Benefit page for retirees for information about available death benefits and how to update your beneficiaries and their contact information.

Visit our How Divorce Can Affect NYSLRS Benefits page for more information, including how divorce can affect service credit, disability benefits or retiree cost-of-living adjustments.

Looking for some summer reading to add to your e-reader? Check out these publications from NYSLRS for important retirement information.

1. Retirement Plan for ERS Tier 6 Members (Article 15)

Are you one of more than 350,000 Tier 6 Employees’ Retirement System (ERS) members covered by Article 15? Your retirement plan publication explains some of the benefits and the services available to you, including service retirement, disability retirement, death benefits and more. Read it now.

2. Retirement Plan for ERS Tier 3 and 4 Members (Articles 14 and 15)

If you’re not in Tier 6, you’re likely among more than 260,000 Tier 3 and 4 ERS members covered by Article 14 and 15. Check out your publication to find out about the benefits and the services available to you. Read it now.

3. Service Credit for Tiers 2 Through 6

The service credit you earn as a NYSLRS member is an important factor in the calculation of your pension. This publication explains the service you can earn credit for and how you can request to purchase credit for additional public employment or military service. Read it now.

4. What If I Leave Public Employment?

While we hope you stay a NYSLRS member throughout your working career, we understand that circumstances can change. If you leave public employment, this publication explains what you’ll need to do and what happens to your NYSLRS membership. Spoiler: It depends on how much service you have. Read it now.

5. What If I Work After Retirement?

Generally, NYSLRS retirees under age 65 can earn up to $35,000 per calendar year from public employers in New York State without affecting their NYSLRS pension. However, you should be aware of the laws governing post-retirement employment and how working after retirement may impact your retirement benefits. If you are considering working while collecting your pension, you should read this publication. If you already work in public employment as a NYSLRS retiree, read our Update Regarding Retiree Earnings Limit blog post for information about recent legislation and Governor’s executive orders that affect the limit.

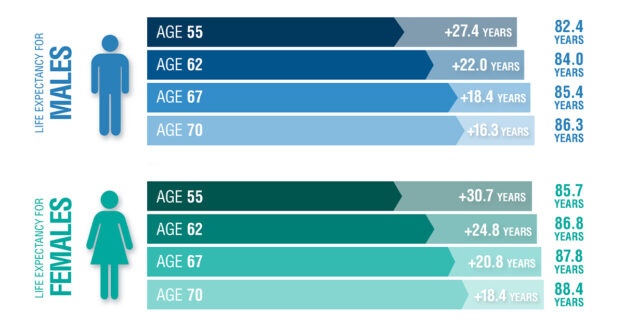

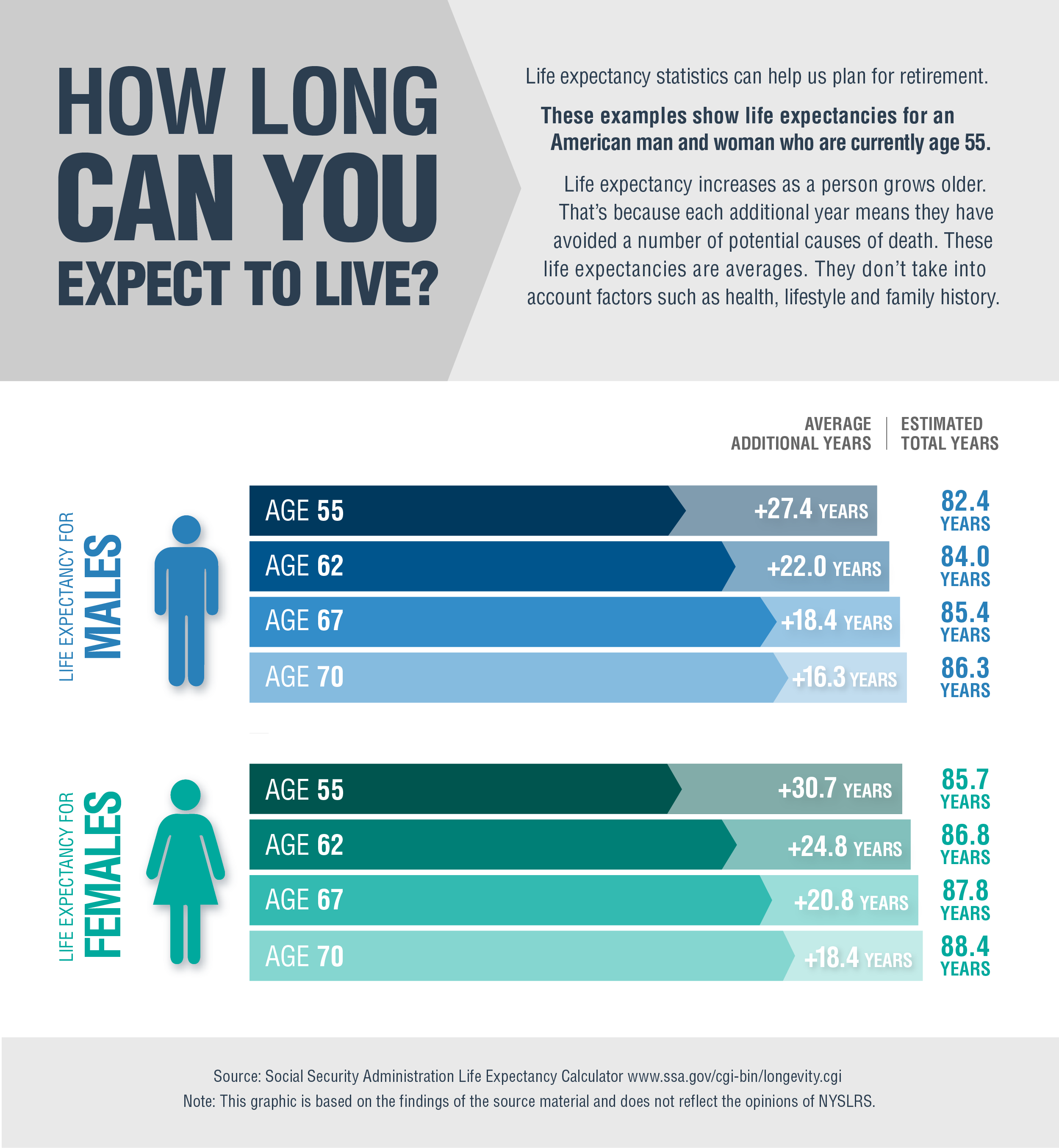

As you plan for retirement, you need to think about your sources of income in retirement. However, you should also consider how long your retirement income will need to last.

Longer Life Span, Longer Retirement

These days, a 55-year-old man can expect to live for another 27.4 years, to about 82. A 55-year-old woman can expect to live for more than 30 years. These figures, derived from the Social Security life expectancy calculator, are only averages. They don’t account for factors such as health, lifestyle or family medical history.

Here are some other statistics worth considering as you plan for retirement (as of the State fiscal year that ended March 31, 2022):

More than 37,000 NYSLRS retirees were over 85 years old;

More than 3,500 had passed the 95-year mark; and

401 NYSLRS’ retirees were 101 or older.

Considering that many public employees can retire as early as 55, it’s possible that a fair number of them could have retirements that last 45 years or more.

Saving for a Long Retirement

Your NYSLRS pension is one source of income that you can depend on however long your retirement lasts. Employees’ Retirement System (ERS) members who retired in fiscal year 2022 are receiving an average monthly pension of $2,748. Social Security is another long-term source. The average Social Security benefit for a retired worker was $1,837 a month, as of June 2023.

Your retirement savings is a crucial asset that can supplement your pension and Social Security. In a long retirement, savings can help with rising costs and provide a source of cash in an emergency.

It is never too late to start saving for retirement. The New York State Deferred Compensation Plan is one easy way to get started. It’s a program created for New York State employees and employees of participating public agencies. If you’re a municipal employee, ask your employer if you’re eligible for the Deferred Compensation Plan or another retirement savings plan. (The New York State Deferred Compensation Plan is not affiliated with NYSLRS.)

You should also visit our Start Saving for Retirement page. You’ll find an example of how much you can save over a 30-year period, and a sample withdrawal strategy designed to provide retirement income for 20 years.

New York Retirement News is dedicated to keeping NYSLRS members and retirees informed about developments that may affect their benefits. In case you missed them, or just want to take another look, here are some of our most popular blog posts from the past year.

Becoming Vested Becoming vested is a crucial milestone in your NYSLRS membership. Under legislation enacted in April 2022, Tier 5 and 6 members are now vested after five years of service. Previously, these members needed ten years of service credit to be eligible for a service retirement benefit.

Update Regarding Retiree Earnings Limit Normally, most NYSLRS retirees who return to work for a public employer are limited in how much they can earn before their pension would be suspended. The limit is $35,000 per calendar year, however, executive orders from the Governor and legislation temporarily suspended this limit. Read the blog post for current information.

Enhanced Death Benefit for Survivors of COVID-19 Victims Survivors of NYSLRS members who contract COVID-19 on the job may be entitled to an enhanced death benefit if the member dies as a result of the disease. This accidental death benefit covers eligible deaths through December 31, 2024.

Find Your Retirement Plan Publication Your retirement plan publication is an essential resource that provides comprehensive information about your NYSLRS benefits. It explains how long you’ll need to work to receive a pension, how your benefit is determined, what death and disability benefits may be available and more. Our new tool can help you find your plan publication.

What is a Defined Benefit Plan? As a NYSLRS member, you are part of a defined benefit plan, also known as a traditional pension plan. Defined benefit plans are often confused with defined contribution plans, but there are major differences between the two types of plans.

Service credit is one of the major factors in calculating your NYSLRS pension. You earn a year of service credit for each year of full-time employment with a participating employer. In some cases, you may also be able to request additional credit for past service, which could increase your pension amount.

You can request credit for past service if you:

Worked for a participating employer before joining NYSLRS;

Worked for a public employer that later participated in NYSLRS; or

Received an honorable discharge from active military duty.

In most cases, you have to pay to receive additional service credit. The sooner you purchase your credit, the less it will generally cost. You must apply for any additional service credit that you wish to receive before you retire. After you apply, we’ll determine whether you’re eligible for the credit and how much it would be.

Credit for Previous Public Employment

Additional service credit includes work for an employer who later joined NYSLRS, or for public employment before you became a NYSLRS member.

Example: You worked at the town library while going to school and, as a part-time employee, you chose not to join NYSLRS. When you graduated and took a full-time job at the Town Supervisor’s office, you were required to join. You can request credit for the part-time service at the library.

When you apply, you’ll be asked for the name of the employer and the approximate dates you worked there. We encourage you to submit any proof you may have of your previous service. We will also reach out to your former employer, but you may be able to expedite the process by providing payroll records such as W-2 forms or pay stubs to NYSLRS when you apply.

You must earn two years of service credit as a member before additional service can be credited to you.

Military Service Credit

If you served in the U.S. armed forces, you may be eligible to purchase credit toward your retirement for your military service, regardless of whether your military service was before or after you joined NYSLRS.

There are different sections of the law that allow credit for military service. The amount of military service credit you can receive, and the cost (if any), will vary depending on which section of the law allows the credit. Reserve and National Guard service may qualify if it’s considered active duty.

For certain military service, you must have five years of member service credit before you can apply.

How to Request Additional Service Credit

You can apply for additional service credit and military service credit in Retirement Online. Sign in to your account, scroll down to the ‘My Account Summary’ section of your Account Homepage and click the “Manage My Service Purchases” button, then click “Request Additional Service Credit.” If you are applying for military service credit, select “Article 20 Military” when asked for your employer.

There may be other ways to increase your retirement service credit. If you had a previous membership in a New York State public retirement system and it was terminated, you may be able to reinstate your membership. If you still have an active membership in another public retirement system, but you are no longer working for the employer that participates in that retirement system, you may be able to transfer that membership to NYSLRS.

A word of caution — there are certain situations where purchasing additional service credit will not increase your pension. For example, special retirement plans for police officers and firefighters allow retirement after 20 or 25 years of service regardless of age, but not all types of public employment count toward the 20 or 25 years in these plans. Contact us if you have questions.

For more information about purchasing additional credit:

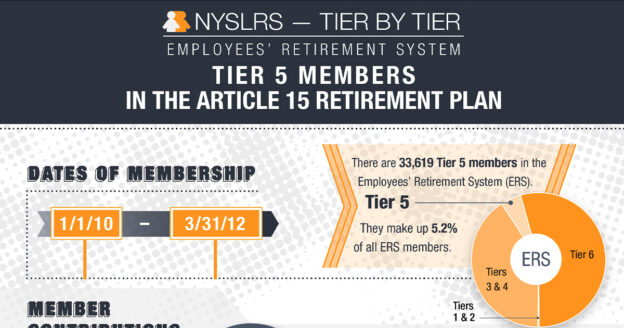

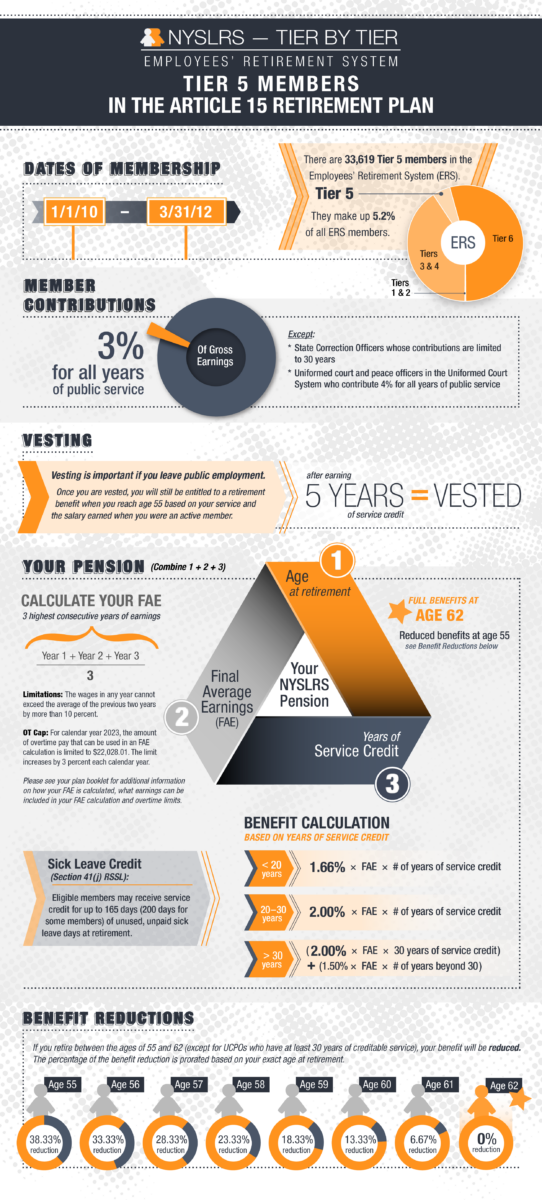

When you joined the New York State and Local Retirement System (NYSLRS), you were assigned a tier based on the date of your membership. This post looks at Tier 5 members of the Employees’ Retirement System (ERS).

Your tier determines such things as your eligibility for benefits, the calculation of those benefits, death benefit coverage and whether you need to contribute toward your benefits.

ERS has six tiers. Anyone who joined from January 1, 2010 through March 31, 2012 is in Tier 5. There were 33,619 ERS Tier 5 members as of March 31, 2022, representing 5.2 percent of ERS membership.

Most ERS Tier 5 members (unless they are in special retirement plans) retire under the Article 15 retirement plan. Check out the graphic below for the basic retirement information for Tier 5 members in this plan.

If you retire with less than 20 years, the benefit is 1.66 percent of your final average earnings (FAE) for each year of service. If you retire with 20 to 30 years, the benefit is 2 percent of your FAE for each year of service. For each year of service beyond 30 years, you will receive 1.5 percent of your FAE. For example, with 35 years of service, you can retire at 62 with 67.5 percent of your FAE.

Where to Find More ERS Tier 5 Information

For more information about ERS Tier 5 membership, find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits provided by your specific plan.

You can check your service credit total and estimate your pension using Retirement Online. Most members can use our online pension calculator to create an estimate based on the salary and service information NYSLRS has on file for them. You can enter different retirement dates to see how your choices would affect your potential benefit.

Members may not be able to use the Retirement Online calculator in certain circumstances, for example, if they have recently transferred a membership to NYSLRS. These members can contact us to request an estimate or use the “Quick Calculator” on our website. The Quick Calculator generates estimates based on information you provide.

For information about other tiers, our series NYSLRS – One Tier at a Time gives you a quick look at the benefits for other tiers in both ERS and the Police and Fire Retirement System.

*Uniformed court officers or peace officers employed by the Unified Court System that have at least 30 years of credit may retire with a full benefit as early as age 55.

Retirement law can be confusing. Sometimes a small misunderstanding can have a big impact on your benefit. That’s why it’s important to correct some common retirement myths. Here are the top five:

Retirement Myth #1

My NYSLRS contributions go into a personal 401(k)-style savings account that I will get when I retire.

NYSLRS is a defined benefit plan. Your pension will be based on your earnings and years of service — it will not be based on your contributions.

Retirement Myth #2

If I work for more than one NYSLRS participating employer, the service credit from both will count toward my pension benefit.

It depends. You can only earn one year of service credit in a 12-month period. If you work part-time for two participating employers, you would receive credit toward retirement from both, up to the maximum of one year. However, if you already work full-time for one NYSLRS employer plus you work part-time for another employer, your part-time job won’t increase your retirement service credit. Also, if you are a full-time employee of a school district, you won’t earn extra service credit if you work during the summer.

Retirement Myth #3

NYSLRS administers health insurance coverage for its retirees.

NYSLRS does not administer health insurance programs. We may deduct premiums from a retiree’s monthly pension benefit to pay for health insurance coverage if their former employer instructs us to do so, but we can’t answer questions about coverage or changes in premium amounts.

The New York State Department of Civil Service administers the New York State Health Insurance Program (NYSHIP) for New York State retirees and some municipal retirees. If you are still working, your employer’s human resources (personnel) office should be able to answer your questions about post-retirement coverage.

Retirement Myth #4

I can take out a NYSLRS loan after I retire.

You need to actively work for New York State or a participating employer to borrow against your retirement contributions. NYSLRS loans are not available to retirees.

Retirement Myth #5

If I’m vested and no longer working for a public employer, NYSLRS will automatically start paying my pension as soon as I’m eligible.

Your pension is not automatic. You must apply for retirement 15 to 90 days before your retirement date. Your retirement date is up to you. Most NYSLRS members can begin collecting their pension as early as age 55. If you retire between age 55 and your full retirement age (62 of 63, depending on your tier and plan), you may face a permanent benefit reduction. If you have left public employment though, your benefit won’t increase after you reach full retirement age, so delaying retirement beyond that point can cost you money.

You can find more answers about your NYSLRS benefits in your retirement plan publication. If you have account-specific questions, please message our customer service representatives using our secure contact form.

One aspect of retirement planning some members may not consider is how a divorce may affect their pension benefit. In New York State, retirement benefits earned by NYSLRS members are considered marital property. So, if you get a divorce, a judge may award your ex-spouse part of your pension. The process for dividing retirement assets after a divorce is complicated, but here is some basic information.

Dividing Pension Benefits After a Divorce

A commonly used formula for distributing pension benefits, established by the State Court of Appeals (the Majauskas formula), provides an ex-spouse with a portion of your pension based on half of the service credit you earned while you were married.

For example, let’s say you worked in your public-sector job for 10 years before you married. Then you got married continued working in public service for another 20 years, and then divorced. After the divorce, you continued working in public service for an additional 10 years. You’d have 40 total years of service credit, but only 20 years of your service was earned during your marriage. Under the Majauskas formula, your ex-spouse would be entitled to the proceeds of half of the service credit you earned during the marriage (10 years of service), or a quarter of your pension.

Other ways to divide pension benefits include a flat dollar amount, a benefit based on a specific date or a flat percentage of the benefit.

Domestic Relations Orders

To divide your retirement benefits after a divorce, NYSLRS needs a Domestic Relations Order (DRO). This court order, issued after a final judgment of divorce, gives us specific instructions on how your benefits should be split.

If your pension benefits will be affected by divorce, your DRO should be submitted to the Retirement System before you apply for retirement. We require a certified copy of the DRO, and it must be signed by a Supreme Court judge and entered as an official court document. We also require proof of divorce, such as a copy of the judgment of divorce. Failure to submit your DRO before you retire could result in a delay of your pension payments or an overpayment to you, which would need to be recovered by NYSLRS.

Learn More

Divorce may affect other NYSLRS benefits as well. Read Divorce and Your Benefits for more information including formulas for determining an ex-spouse’s share, a template you can use to draft a DRO and how to avoid a rejected DRO.