Over the past century, NYSLRS has provided pension security for retired public workers, whose spending has contributed to the economic strength and stability of their communities.

In every corner of the Empire State, NYSLRS retirees shop at local stores and patronize local businesses, which in turn helps create jobs. NYSLRS retirees also pay a significant share of local taxes.

Economic Stability

Spending by NYSLRS retirees provides something else for their communities: economic stability.

Because a NYSLRS pension is a defined-benefit retirement plan, retirees and beneficiaries receive a guaranteed monthly payment for life. Defined-benefit plans, which pay benefits based on a pre-set formula, differ from defined-contribution plans, such as a 401k, which are essentially retirement savings accounts.

Recipients of defined-benefit plans don’t have to worry about their money running out during retirement or a drop in their monthly income because of a dip in the stock market. They are better able to maintain their spending during economic downturns, which helps local businesses stay afloat during hard times.

That stability is particularly important in rural parts of the State, which are more susceptible to downturns because they lack the economic diversity of more-urban areas.

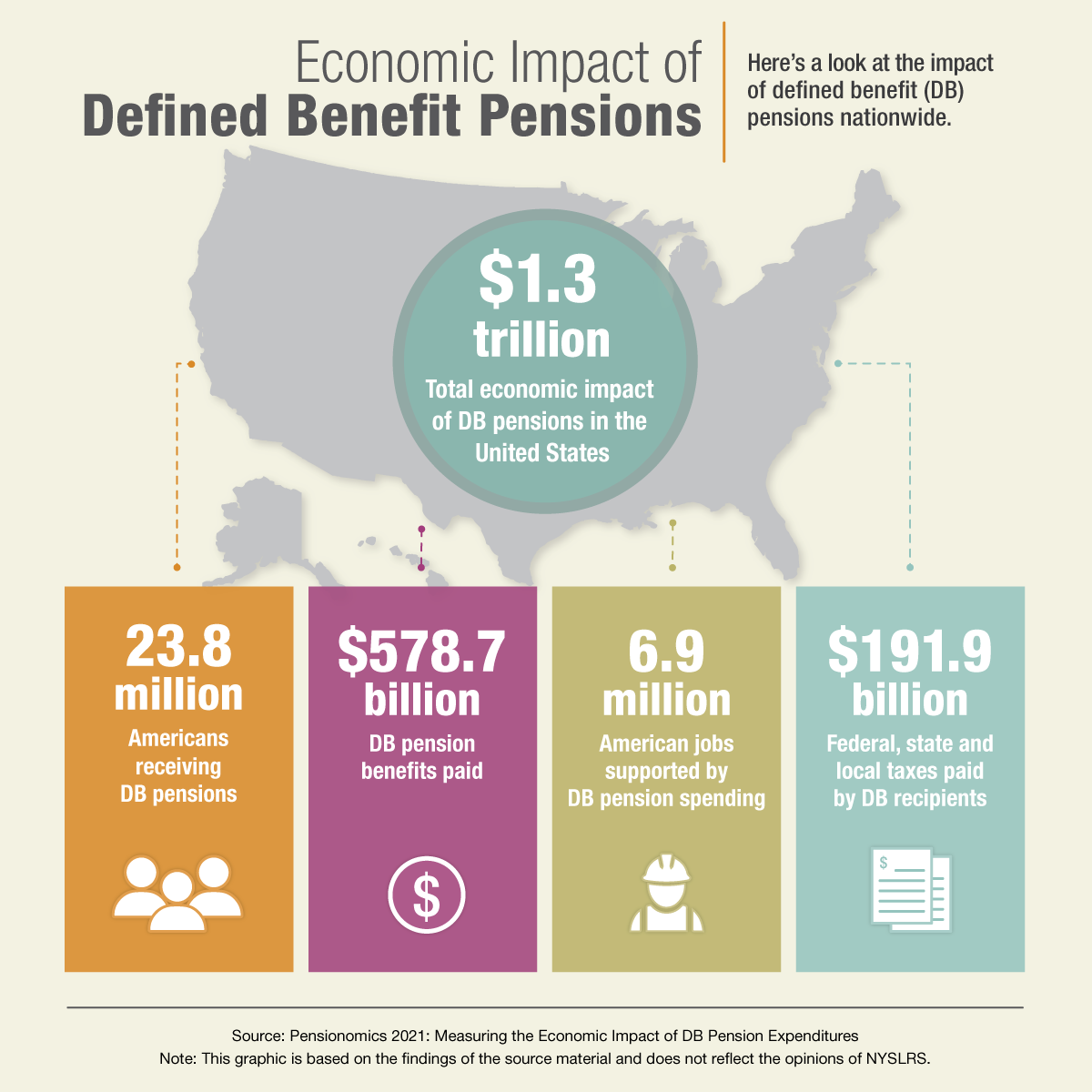

Defined-benefit pensions don’t just help New York State. Across the nation, these pensions are benefitting millions of pensioners and their communities. In 2018, defined-benefit pension plans paid $578.7 billion to 23.8 million retired Americans, and their spending supported 6.9 million jobs and generated $1.3 trillion in economic activity, according to a study by the National Institute on Retirement Security (NIRS).

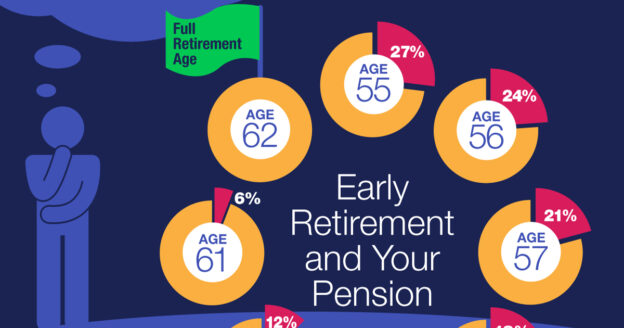

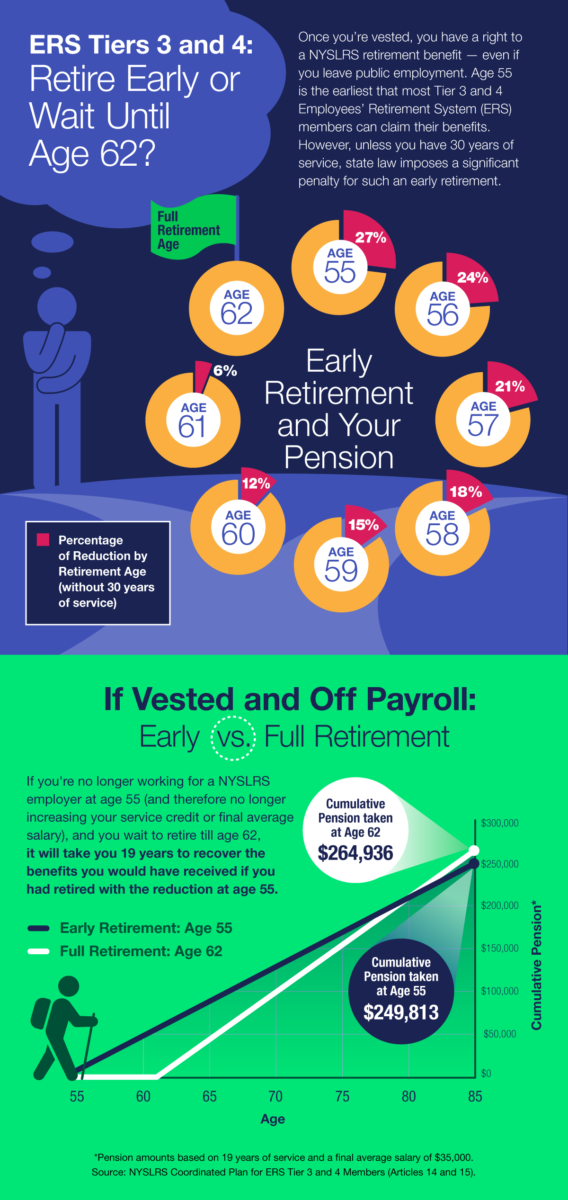

Tier 3 and 4 members in the Article 15 retirement plan qualify for retirement benefits after they’ve earned five years of credited service. Once you’re vested, you have a right to a NYSLRS retirement benefit — even if you leave public employment. Though your pension is guaranteed, the amount of your pension depends on several factors, including when you retire. Here is some information that can help you determine the right time to retire.

Three Reasons to Keep Working

Tier 3 and 4 members can claim their benefits as early as age 55, but they’ll face a significant penalty for early retirement – up to a 27 percent reduction in their pension. Early retirement reductions are prorated by month, so the penalty is reduced as you get closer to full retirement age. At 62, you can retire with full benefits. (Tier 3 and 4 Employees’ Retirement System (ERS) members who are in the Article 15 retirement plan and can retire between the ages of 55 and 62 without penalty once they have 30 years of service credit.)

Your final average earnings (FAE) are a significant factor in the calculation of your pension benefit. Since working longer usually means a higher FAE, continued public employment can increase your pension.

The other part of your retirement calculation is your service credit. More service credit can earn you a larger pension benefit, and, after 20 years, it also gets you a better pension formula. For Tier 3 and 4 members, if you retire with less than 20 years of service, the formula is FAE × 1.66% × years of service. Between 20 and 30 years, the formula becomes FAE × 2.00% × years of service. After 30 years of service, your pension benefit continues to increase at a rate of 1.5 percent of FAE for each year of service.

If You’re Not Working, Here’s Something to Consider

Everyone’s situation is unique. For example, if you’re vested and no longer work for a public employer, and you don’t think you will again, taking your pension at 55 might make sense. When you do the math, full benefits at age 62 will take 19 years to match the money you’d have received retiring at age 55 — even with the reduction.

An Online Tool to Help You Make Your Decision

Most members can use Retirement Online to estimate their pensions.

A Retirement Online estimate is based on the most up-to-date information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit, which could help you determine the right time to retire. When you’re done, you can print your pension estimate or save it for future reference.

If you are unable to use our online pension calculator, please contact us to request a pension estimate.

This post has focused on Tier 3 and 4 members. To see how retirement age affects members in other tiers, visit our About Benefit Reductions page.

Defined benefit pension plans, including NYSLRS, provide retirement security for millions of Americans. Here in New York, NYSLRS pays out more than $10 billion in benefits each year to nearly 400,000 New York State residents. Much of that money is spent at home, contributing to local economies and supporting jobs.

What’s happening here is mirrored across the country. According to a study released by the National Institute on Retirement Security (NIRS) in 2021, defined benefit pension plans paid $578.7 billion to 23.8 million retired Americans, and those payments had a significant impact on the nation’s economy.

What Is a Defined Benefit Pension Plan?

A defined benefit pension plan provides a pension that is based on a preset formula that takes into account salary and years of service. Unlike a 401(k)-style retirement plan (also known as defined contribution plan), it is not based on how much you or your employer contribute to your retirement account. A defined benefit plan provides a fixed monthly payment at retirement and is usually a lifetime benefit.

With a defined contribution plan, the amount of money the employee has accumulated at retirement depends on the investment returns of their individual account. A market downturn, especially near retirement, can affect the value of their benefit. With a defined benefit plan, market risk is shared, so a downturn doesn’t affect the benefit.

Most importantly, defined benefit pension recipients don’t have to worry about their money running out during their retirement years.

Who Gets Defined Benefits?

Defined benefit pension plans were once much more common in the United States. Today, defined benefit plans are more commonly offered by public employers, though about 16 percent of full-time private sector employees had access to a define benefit plan in 2018.

Who received these benefits? According to the NIRS study:

$308.7 billion was paid to 11 million state and local government retirees and beneficiaries;

$105.9 billion was paid to 2.6 million federal retirees and beneficiaries; and

$164.1 billion was paid to 10.1 million private sector retirees and beneficiaries.

Employers Benefit from Defined Benefit Plans

Not surprisingly, the financial security provided by defined benefit plans has proved popular among workers. In 2019, the NIRS surveyed 1,100 public employees about their benefits. Most said retirement benefits are good tools for recruiting and retaining workers, and 86 percent said their retirement benefits are a major reason they stick with their jobs.

National Economic Benefits of Defined Benefit Plans

The $578.7 billion in pension payments generated spending that supported 6.9 million American jobs with paychecks totaling $394.2 billion, the study estimated. But the economic benefit didn’t stop there. This is because of what economists call the multiplier effect, the measure of the true impact of each dollar spent as it works its way through the economy.

The study found that each pension dollar paid had a $2.19 multiplier effect, which resulted in nearly $1.3 trillion in economic output. Real estate, food service, healthcare, and wholesale and retail trade were the sectors most impacted.

The study also noted that defined benefit pension payments have a stabilizing effect on local economies. Because they have a steady source of income, retirees with a defined benefit plan are less likely than retirees with defined contributions to curtail spending during economic downturns.

“These plans are a cost effective way to provide secure lifetime income for retired Americans and their beneficiaries after a lifetime of work. Moreover,” the study concluded, “DB pension plans generate economic benefits that reach well beyond those who earned benefits during their working years.”

As a NYSLRS member, you have a defined benefit retirement plan that provides a lifetime pension when you retire. The formula used to calculate these benefits is based on two main factors: service credit and final average earnings. You’re probably familiar with service credit — it’s generally the years you’ve spent working for a participating employer. But what are final average earnings (FAE)?

When we calculate your pension, we find the set of consecutive years (one, three or five, depending on your tier and retirement plan) when your earnings were highest. The average of these earnings is your FAE. Usually your FAE is based on the years right before retirement, but they can come anytime in your career. The years used in determining your FAE do not necessarily correspond to a calendar year. For FAE purposes, a “year” is any period when you earned one full-time year of service credit.

Types of Final Average Earnings

Your tier and plan determine how your final average earnings is calculated:

Three-year FAE: Members in Tier 1, 2, 3, 4 and 5.

Five-year FAE: Members in Tier 6.

One-year FAE: Members in the Police and Fire Retirement System (PFRS). Your employer must choose to offer this benefit. It’s not available to PFRS members covered by Article 14 and generally not available to PFRS Tier 6 members.

If you are not sure what retirement plan you are in, you may want to read our recent blog post.

Exclusions and Limits

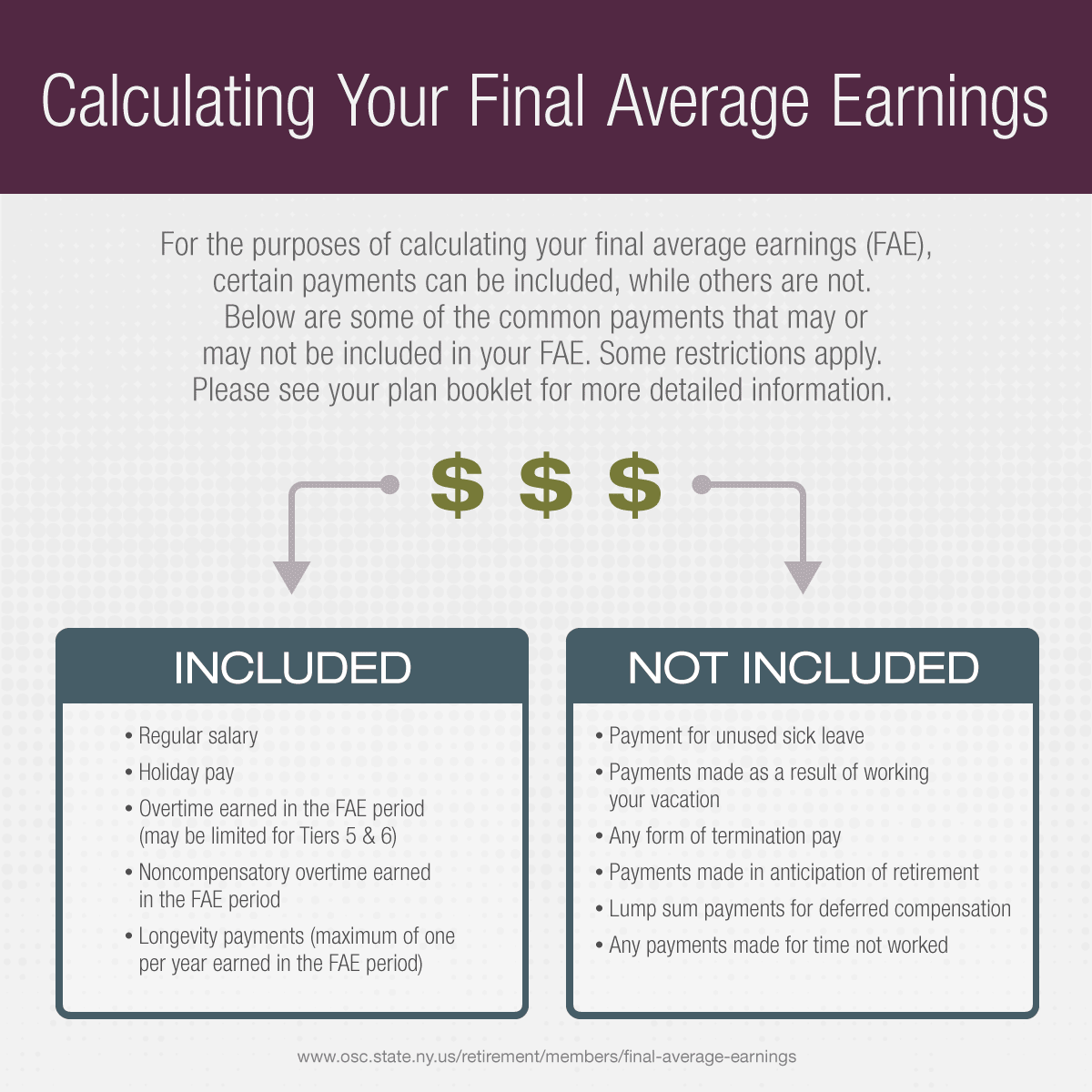

The law limits the final average earnings of all members who joined on or after June 17, 1971. For example, for most members, if your earnings increase significantly through the years used in your FAE, some of those earnings may not be used toward your pension. The specific limits vary by tier; check your retirement plan booklet on our Publications page for details.

Since 2010, with the creation of Tiers 5 and 6, the Legislature and the Governor have introduced additional limits to the earnings that can be used toward the FAE:

Tier 5

Overtime pay is capped — For Employees’ Retirement System (ERS), $20,763.51 in 2021. For PFRS, the cap is 15 percent of earnings.

Tier 6

Overtime pay is capped – For ERS, $17,301 in 2021. For PFRS, the cap is 15 percent of earnings.

Lump sum vacation pay and wages from more than two employers are no longer included in your FAE.

Any earnings above the Governor’s salary cannot be included in your FAE.

Calculating Your Final Average Earnings

Your final average earnings is based on money earned during the period used to calculate your pension. This may include payments you receive after you retire, such as retroactive pay from a contract negotiation or pay for unused vacation days.

Calculating your FAE at retirement can take time because we must collect salary information from your employer(s) and factor in items such as retroactive payments and earnings you receive after your date of retirement. This is necessary to ensure that your pension calculation is accurate and that you receive all the benefits you are entitled to.

Most NYSLRS members contribute a percentage of their earnings to the Retirement System. Over time, those contributions, with interest, can add up to a tidy sum. But what happens to that money? Will you get your contributions back when you retire? The answer to that question is “no.” Let’s look at what happens to your NYSLRS contributions.

How NYSLRS Retirement Plans Work

NYSLRS plans are defined benefit pension plans. Once you’re vested, you’re entitled to a lifetime benefit that will be based on your years of service and final average earnings. The amount of your contributions does not determine the amount of your pension. (Use Retirement Online to estimate your pension.)

Your NYSLRS plan differs from defined contribution plans, such as a 401-k plan, which are essentially retirement savings plans. In those plans, a worker, their employer, or both contribute to an individual retirement account. The money is invested and hopefully accumulates investment returns over time. This type of plan does not provide a guaranteed lifetime benefit and there is the risk that the money will run out during the worker’s retirement years. Experts recommend that workers who have defined contribution plans contribute anywhere from 10 to 20 percent of their income to their plan. NYSLRS members, in contrast, contribute between 3 and 6 percent of their income, depending on their tier and retirement plan.

Where Your Contributions Go

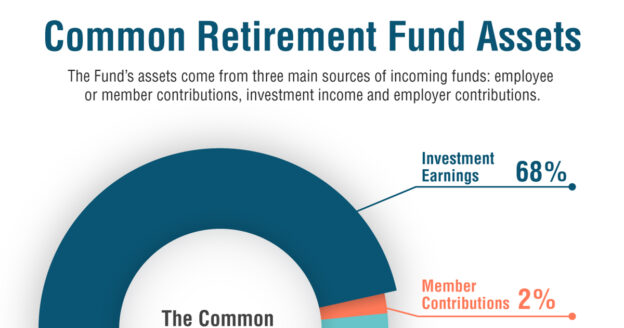

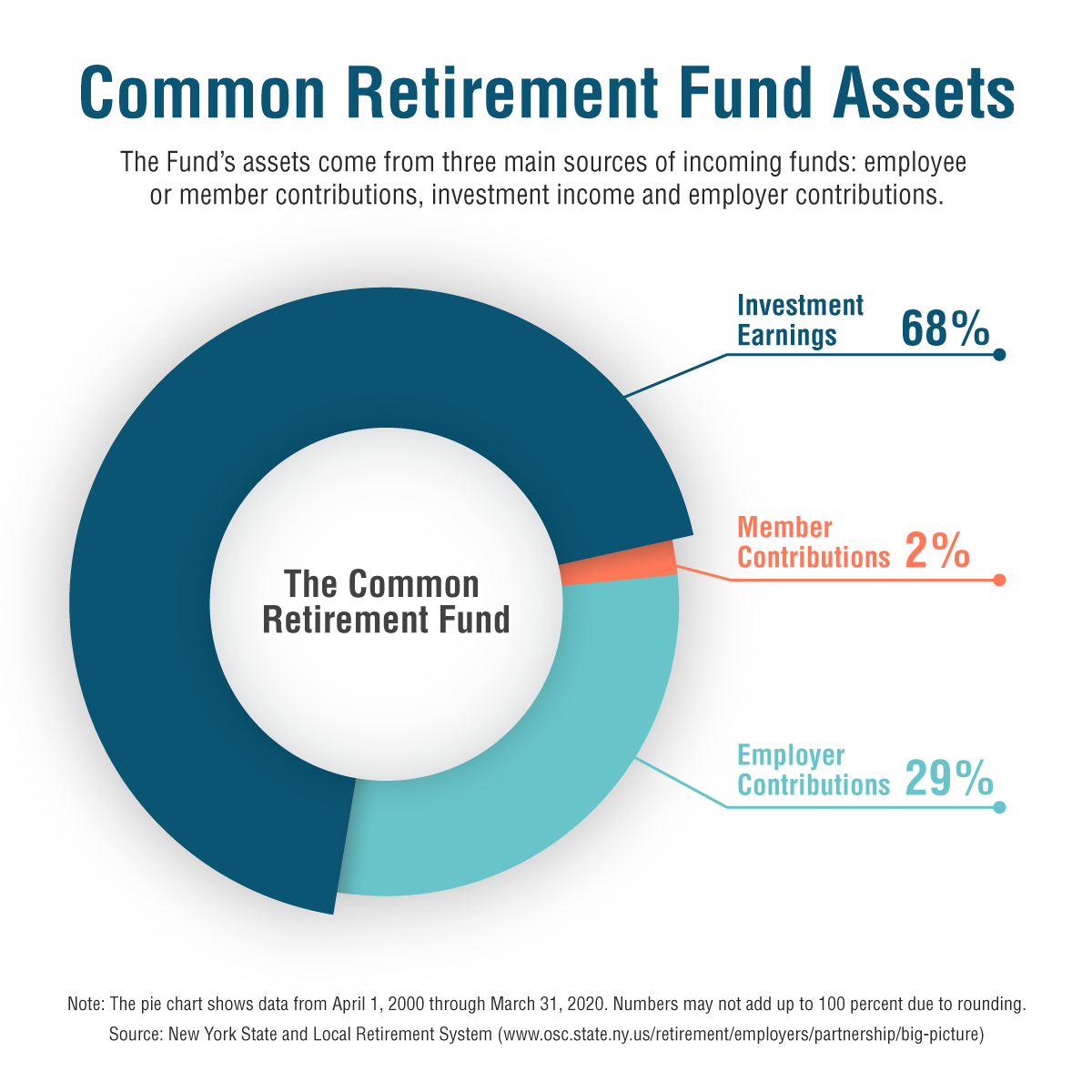

When you retire, your contributions go into the New York State Common Retirement Fund. The Fund is the pool of money that is invested and used to pay retirement benefits for you and other NYSLRS members.

Your Contribution Balance

You can find your current contribution balance in Retirement Online. But if your contributions don’t determine your pension, what difference does it make what the balance is? For one thing, your contribution balance helps determine the amount you can borrow if you decide to take a loan from NYSLRS. Also, you may be able to withdraw your contributions, with interest, if you leave the public workforce before retirement age.

Withdrawing Your Contributions

You cannot withdraw your contributions while you are still working for a public employer in New York State. If you leave public employment with less than ten years of service, you can withdraw your contributions, plus interest. If you withdraw, you will not be eligible for a NYSLRS retirement benefit.

If you have more than ten years of service, you cannot withdraw, but you will be entitled to a pension when you reach retirement age. But remember, you will not receive this pension automatically; you must file a retirement application before you can receive any benefit.

When should you start saving for retirement? If you aren’t saving already, right now is the best time to start. If your retirement is a long way off, that means you’ll have more time for your savings to grow. But even if you’re close to retirement, it is never too late to start saving.

Why Save for Retirement?

While retirees tend to spend less than they did while they were working, financial experts say you’ll still need 70 to 80 percent of your pre-retirement income to maintain your lifestyle during retirement.

NYSLRS members have the rare advantage of a well-funded, defined-benefit pension. As a NYSLRS member, once you’re vested, you’re entitled to a pension that, once you retire, will provide you with monthly payments for the rest of your life. Retirement savings can supplement your NYSLRS pension and Social Security, helping you reach that income-replacement goal.

Retirement savings can also be a hedge against inflation and a source of cash in an emergency. A healthy retirement account will give you more flexibility during retirement, helping ensure that you’ll be able to do the things you want to do. It can also provide peace of mind.

Getting Started

For New York State employees and many other NYSLRS members, there’s an easy way to get started. If you work for a participating employer, you can join the New York State Deferred Compensation Plan. If you don’t work for New York State, check with your employer to see if you are eligible. If you are not eligible, your employer may be able to direct you to an alternative retirement savings program.

Once you sign up for Deferred Compensation, your contributions will automatically be deducted from your paycheck and deposited into your account. You can choose from a variety of investment packages or choose your own investment strategy. (The Deferred Compensation Plan is not affiliated with NYSLRS.)

The New York State and Local Retirement System (NYSLRS) consists of two retirement systems: the Employees’ Retirement System (ERS) and the Police and Fire Retirement System (PFRS). Your job title determines what system you’re in. In some cases, however, it’s possible to have a dual membership, to be a member of both systems.

How Does Dual Membership Work?

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines your tier in each membership.

Implications of Dual Membership

As a member of both systems, you’d have separate membership accounts. Let’s look again at our fire-fighting bus driver example. While working as a firefighter, you make any required contributions and earn service credit toward your PFRS pension only. The same is true for your work as a bus driver—your required contributions and earned service credit only go toward your ERS pension, not your PFRS pension.

There are other implications to dual membership. Assuming you’re vested in both memberships and meet the service credit and age requirements, you could retire and collect a pension from both systems. You’d need to file separate retirement applications for ERS and PFRS, and we’d calculate each pension separately. We’d calculate your ERS pension using the final average earnings (FAE) you earned as a bus driver and your PFRS pension using the FAE from your time as a firefighter.

And, since you’d have both an ERS pension and a PFRS pension, you would need to choose a beneficiary for each in the event of your death.

Questions?

You’ll want to make sure to know the details of your retirement plan in each system. If you have questions about dual membership, or want to discuss your particular situation when you decide to retire, please contact us.

The COVID-19 pandemic has caused economic uncertainty as well as a public health emergency. Businesses are struggling, more people are unemployed, and markets are volatile. Yet among all the uncertain news we seem to hear daily, there is something NYSLRS members and retirees can have confidence in: your Retirement System and pension fund are strong and secure.

Since it was established in January 1921, NYSLRS has proven its strength and durability. Over the past century, the Retirement System has weathered the Great Depression of the 1930s, the Dotcom bubble burst of 2001, the Great Recession of 2008-2009 and more than a dozen other economic downturns. Each time, NYSLRS recovered and emerged stronger than before.

Investing for the Long Term

The New York State Common Retirement Fund, which holds and invests the Retirement System’s assets, has been impacted by this largely unprecedented crisis, but the Fund remains strong. While weighing the risk and benefit of every investment, the Fund employs a diversified investment strategy that is designed for the long-term, allowing it to take advantage of growth opportunities in good times, which helps it to better navigate through hard times.

NYSLRS entered the current crisis in a position of strength. Independent analysts, such as the Pew Charitable Trusts, have long recognized NYSLRS as one of the best-managed and best-funded public retirement systems in the nation. The strength of the Fund provides stability and enhances its ability to recover from market swings.

In recent months, before the COVID-19 outbreak, the Fund’s professional managers recognized increased volatility in the stock market. The managers made adjustments in the Fund’s investment portfolio in preparation for an expected economic downturn and are actively managing the Fund through these difficult times. The Fund has more than enough assets to pay retiree benefits.

What This Means for You

New York State Comptroller Thomas P. DiNapoli has a fiduciary responsibility to manage the Fund’s assets on behalf of NYSLRS members and retirees. Protecting the Fund is the Comptroller’s number one priority. As a NYSLRS member or retiree, your lifetime retirement benefits are guaranteed by the State constitution, and those benefits cannot be diminished.

NYSLRS continues to be well-positioned to meet both its short-term and long-term obligations. If you are already retired, you will continue to receive your pension payments on schedule. If you are a member, your pension will be there for you when you retire and throughout your retirement years.

We’ve faced similar challenges in the past. We will get through this one.

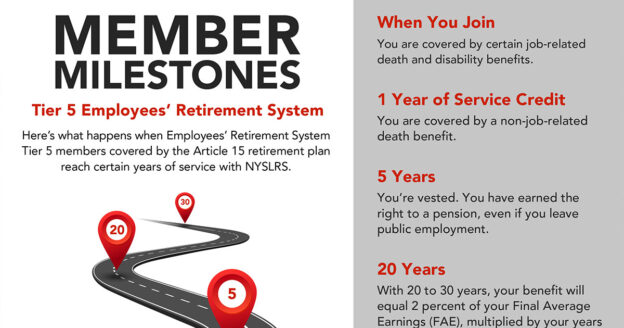

If you joined the Employees’ Retirement System (ERS) on or after January 1, 2010, but before April 1, 2012, you are a Tier 5 member. Let’s look at the milestones you will pass over the course of your public service career and how they will affect your benefits.

Why Milestones Matter

As a NYSLRS member, you earn service credit for your paid public employment. Generally, one year of full-time work equals one year of service credit. Certain amounts of service are milestones because they affect the benefits you receive and how your pension will be calculated. A better understanding of when they occur and how they change your benefits will help you plan for retirement.

Your milestones depend on your tier and your retirement plan. Most ERS Tier 5 members will retire under the Article 15 retirement plan. Some ERS Tier 5 members, such as deputy sheriffs and state corrections officers, are in special plans. You can find information for the Article 15 plan and other Tier 5 plans in your NYSLRS retirement plan publication.

Major

Milestones for Tier 5

Here are some important milestones for Tier 5 members in the Article 15 retirement plan:

With ten years of service credit, you can apply for a non-job-related disability benefit if you are permanently disabled and cannot perform your duties because of a physical or mental condition.

With ten years of service credit, your beneficiaries may be eligible for an out-of-service death benefit if you leave public employment and die before retirement.

Ten years also marks the point when you are no longer able to withdraw your membership and receive a refund of your contributions if you leave public employment.

You are eligible to retire once you are age 55 and have five years of service credit. However, for most Tier 5 members, there would be reductions to your benefit if you retire before age 62.

You can retire with full benefits at age 62.

If you retire with fewer than 20 years of service, your pension will equal 1.66 percent of your final average earnings (FAE) for each year of service.

With 20 to 30 years of service credit, your benefit will equal 2 percent of your FAE for each year of service.

Then, for each year of service beyond 30 years, you will receive 1.5 percent of your FAE.

Note: The law limits the final average earnings of all members who joined on or after June 17, 1971. For example, for most members, if your earnings increase significantly during the years used in your FAE, it’s possible that some of those earnings may not be used toward your pension. The specific limits vary by tier. Visit our Final Average Earnings page for more information.

The amount of your pension also depends on several factors, including your years of service credit and your age when you retire. Most members can estimate your pension in Retirement Online and enter different retirement dates to see how those choices would affect your benefit. As of April 9, 2022, Tier 5 and 6 members only need five years of service credit to be vested. If you are a Tier 5 or 6 member with between five and ten years of service credit, you can contact us to request a benefit estimate.

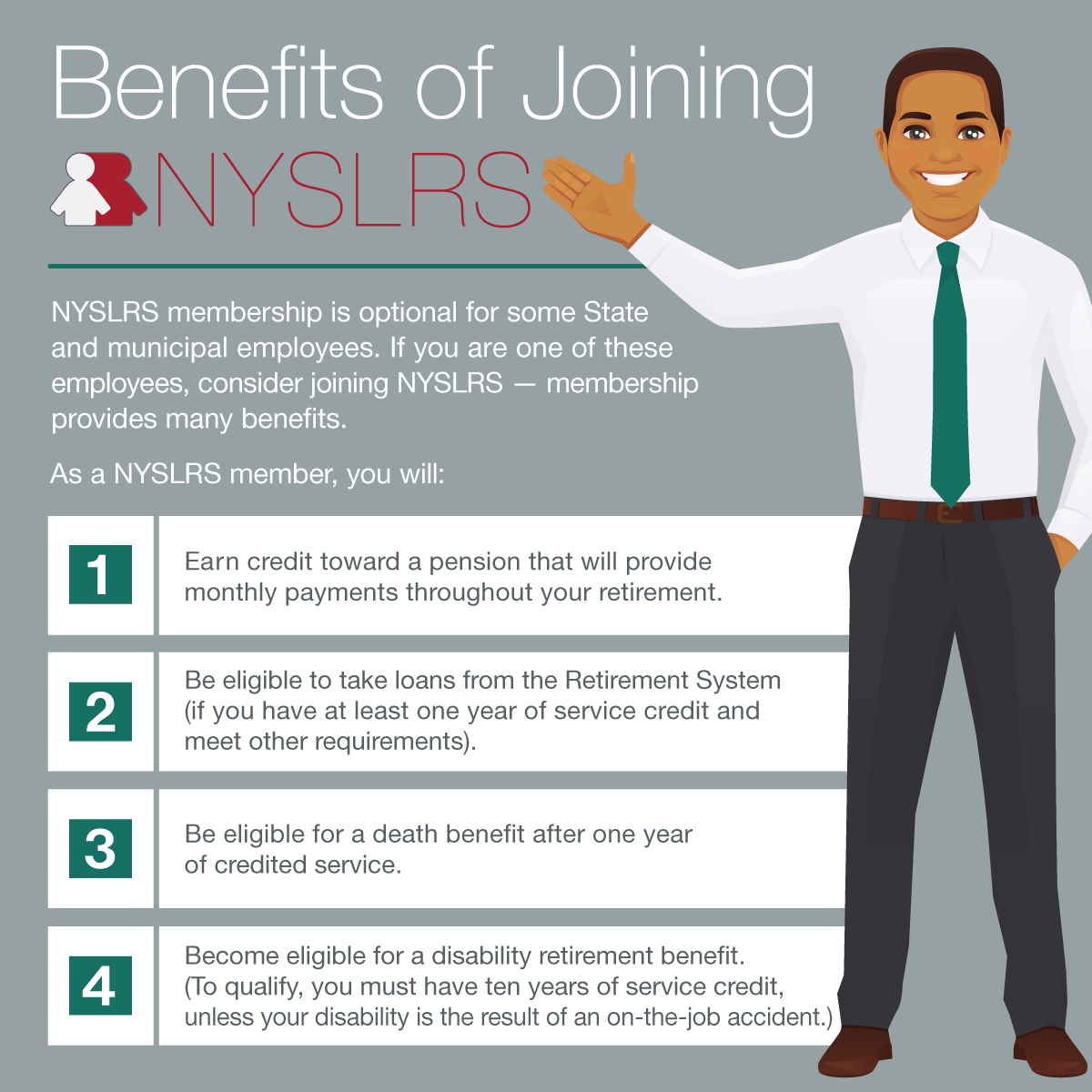

Most State and municipal employees are required to join the New York State and Local Retirement System (NYSLRS) when they are hired. But for some employees, such as part-time and seasonal workers, membership is optional. If you’re a member and you know someone who could join NYSLRS, consider sharing this piece with them.

What is

NYSLRS?

NYSLRS is the third largest retirement system in the nation,

with more than 1.1 million members, retirees and beneficiaries. State

Comptroller Thomas P. DiNapoli administers the Retirement System and is trustee

of the New York State Common Retirement Fund, which holds and invests NYSLRS

assets. The Fund had a value of $210.5 billion as of March 31, 2019.

Why Join NYSLRS?

Joining NYSLRS will improve your chances of a secure

financial future. You’ll earn credit toward a pension that will provide monthly

payments throughout your retirement. But NYSLRS also provides other important

benefits.

What Does

NYSLRS Offer?

As a NYSLRS member, you’ll be eligible for a pension after you earn ten years of service credit. (This is called being vested.) If you work part-time, service credit is pro-rated. For example, if you work half of the hours that a full-time employee works, you’ll receive six months credit for every year you work.

Also, as a NYSLRS member you’ll be able take loans from your

contributions if you’ve earned a year of service credit and meet other

requirements. You’ll be eligible for a death benefit once you have one year of service

credit, and disability benefits after you have ten years of service credit. (If

your disability results from an on-the-job accident, not due to your own

willful negligence, there is no minimum service requirement.)

Over 3,000 employers participate in NYSLRS, allowing you to

continue to build on your benefits if you go to work for another government

employer. Your benefits also may be transferable to six other public retirement

plans in New York.

Making Contributions

As a Tier 6 member, you’ll contribute between 3 and 6

percent of your earnings to the Retirement System. Tier 6 contribution rates

vary based on each member’s annual compensation. If you don’t join NYSLRS when

you first start working and later decide to purchase your previous service

credit, you will need to contribute 6 percent of those earnings plus interest,

even if your salary level for the prior time period would have resulted in a

lower contribution rate.

Your NYSLRS pension will be based on your service credit and

salary, not on the amount you contribute. A NYSLRS pension is a lifetime

benefit. Unlike a 401-k, there is no risk that your pension benefits will be

reduced during your retirement.

But what if you join NYSLRS and decide to leave public

service before you are vested? You won’t lose your contributions. In fact, you

can withdraw your accumulated contributions, plus interest, and roll that money

into a retirement savings plan at your new job.

More Information

If you would like to join NYSLRS or just want more information, please contact your employer’s human resources (personnel) office. You may also be interested in our booklet, Membership in a Nutshell.

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines